99. Interest On Deposits

Description

This section is from the book "Money And Banking", by John Thom Holdsworth. Also available from Amazon: Money And Banking.

99. Interest On Deposits

As a general rule banks do not pay interest on general or demand deposits. Many trust companies, and in recent years commercial banks also, do allow a low rate of interest on daily balances where the average is above a certain minimum. Not a little controversy has arisen regarding the paying of interest on general deposits. The arguments for and against the practice may be briefly summarized.1

In favor of paying interest it is urged that the bank should share with the depositor the profits earned on his deposit. Since the deposits constitute the principal source of the bank's loanable funds and consequently profit, it is contended that the bank should share with the depositors a portion of the profits. Trust companies and private banks pay interest on deposits; commercial banks must do likewise in order to get and hold them. Because the trust companies have for years paid interest on deposits, many of their accounts being inactive, many people have the habit of dividing their bank accounts, banking the most of their funds with a trust company, and keeping with the commercial bank only such balances as are necessary for their daily business needs. To meet this competition of trust companies for deposits, commercial banks more and more find it necessary to pay interest. Again it is urged that since banks demand interest on their deposits kept in other banks, the customer should likewise receive interest for it is his deposits, or a portion of them, that the bank deposits with the correspondent bank.

Against paying interest on deposits it is claimed that if banks engage to pay interest they will take greater risks in lending them in order to earn the interest that must be paid to the depositor. It is further urged that if banks have to pay interest they will not do as much to accommodate depositors in lending them money. As noted elsewhere banks perform many business and financial services for their customers. Not the least of these is accommodating them with loans, so far as their average deposit, financial credit and the securities or collateral offered may warrant. When money is scarce and interest rates advance, banks often continue to lend to large depositors, who are also large borrowers, at the old rates because they keep large balances. If depositors demand interest on their balances, the bank would seem justified in charging the highest rate of interest when they apply for loans or renewals. The growing practice among business houses of selling their notes through bill brokers, thus lessening somewhat their dependence upon the banks for loan accommodations, may have strengthened the tendency to require the payment of interest on deposits.

1 Bolles: Money, Banking, And Finance, p. 69.

Quite generally banks pay interest on public deposits, that is deposits of public funds made by the financial departments of states, cities, counties and school boards. Not infrequently such deposits, or a portion of them, are left undisturbed for considerable periods or are drawn upon only at regular intervals. A bank can, therefore, lend them to good advantage and so can afford to pay interest. Furthermore, banks are not called upon to make loans and extend other favors to municipalities and governments as in the case of the ordinary depositor.

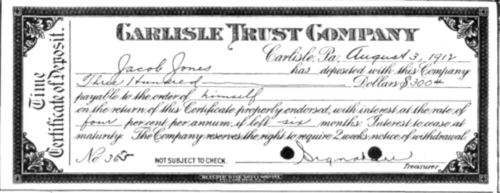

A form of special deposit upon which banks generally pay interest is represented by the certificate of deposit. This instrument certifies that a specified sum of money has been deposited and will be paid to the order of the depositor. It is in effect a check by a bank on itself, and being made payable to the depositor's order may be indorsed by him and so pass from hand to hand like an ordinary check. A certificate may be payable on demand or at the end of a specified period. Demand certificates are sometimes used to transmit money in the same way as bank drafts and certified checks. The depositor is sometimes requested to write his name on the margin of the certificate so that when it is presented for payment, the indorsement, if it has been transferred, can be compared with his signature.

Certificate of Deposit.

Continue to:

My Books