The Land Contract

Description

This section is from the book "The Better Homes Manual", by Blanche Halbert. Also available from Amazon: The Better Homes Manual.

The Land Contract

Another, and a more widely used, financing plan for home buyers in the third group is founded on the land contract. This instrument is most popular in the Middle Western States. It is simply an agreement between the buyer and the seller of property under the terms of which the buyer usually makes a small down payment and agrees to pay the full purchase price in installments, frequently monthly. The seller does not immediately pass the legal ownership of the property to the buyer, but agrees to convey the title to him when a certain percentage of the purchase price, say, 50 per cent, has been paid, at which time the buyer gives a mortgage to the seller or to some third party supplying a loan for the unpaid balance.1

It is said in favor of the land-contract sales method that it makes home ownership possible for a large class of persons who might be unable to buy in any other way. Many real-estate operators like it for the reason that under it they retain the title until the buyer has a substantial equity, and therefore are often in a better legal position than the holder of a mortgage would be in cases where the buyer fails to live up to his agreement.

However, in many cases the land contract has disadvantages to both parties concerned. It is pointed out that the seller may legally contract to transfer title to property which he does not own when the contract is executed, expecting to acquire it prior to the time agreed for the conveyance, and that one who deals with an irresponsible seller contracting on this basis and unable to acquire the property he has agreed to convey may sustain a considerable loss. This situation has sometimes arisen in transactions involving the sale of building lots in new developments. While it is true that the purchaser may often guard against such a contingency by making sure that the seller has a good title and by recording the contract, it is not customary for buyers on land contract to obtain an abstract of title or a certificate of title insurance prior to the time for actual transfer of title, and in some states no provision is made for recording the contract.

1 In a number of states a land contract covering the difference between the down payment and the first mortgage is often used in place of a second mortgage.

[Note. - Excellent amortization tables are included in the pamphlet Present Home Financing Methods from which the foregoing information has been taken.]

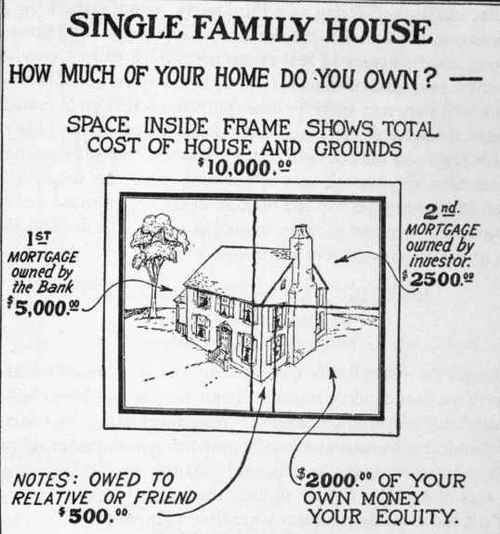

Cracks In Class Mark Off Size Of Interest In House Owned By Others Your Equity Is What Is Left After Others Are Repaid.

Fig. 4. - The proportion of your house that you own is the part you have paid for - your Equity. All the sections in this diagram except the lower right-hand corner represent the shares which others own, although the title may be in your name. (Reprinted from Primer of Housing. Courtesy of Arthur Holden, and Workers Education Bureau Press.)

Again, an unreliable seller might transfer the property to the buyer encumbered with debts much larger than the amount due under the contract, and in this instance the buyer would be compelled to assume obligations not contemplated by his agreement in order to retain the property. Such losses are often prevented by placing the deed in the hands of a bank or similar institution, acting as a third party, which applies the buyer's payments properly and delivers the deed to him at the time agreed upon. Among disadvantages to real-estate men which cause many of them not to enter into land contracts is the fact that a considerable amount of capital which they may need for other purposes is tied up in financing the purchaser. In some places real-estate operators are unable to borrow on favorable terms on the strength of their land contracts, or are unable to sell them at a satisfactory rate of discount. In some states sellers are deterred from using the method because of the complicated and lengthy legal procedure required in cases where the buyer defaults and the seller wishes to regain possession of the property.

Continue to:

My Books