Loan Ratios As Business Barometers

Description

This section is from the book "Banking Principles And Practice", by Ray B. Westerfield. Also available from Amazon: Banking principles and practice.

Loan Ratios As Business Barometers

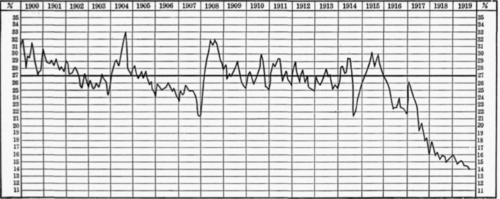

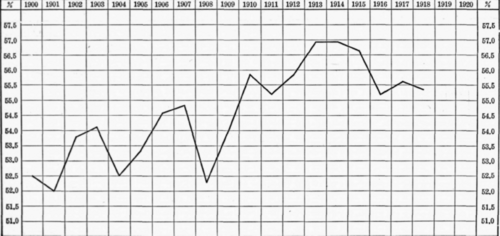

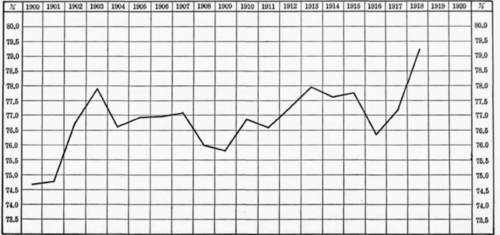

The sum of a bank's investments in securities and of its loans and discounts represents its contributions of capital to business. A part of these funds was originally deposited as cash in the bank; the rest have been created by the bank. Bank notes and deposit liabilities have been created and exchanged by the bank for various credit items of borrowers, while the borrowers possessing these bank notes, deposits, or actual government money, have been enabled to procure materials, labor, tools, plant, transportation, and the like. The funds put into investments and some indeterminate proportion of the loans (and discounts) represent contributions of permanent capital. The proportion of the loans which constitutes permanent advances of capital ranges in all probability from 20 to 50 per cent. The tendency is to increase. The ratio of cash reserve to investments, plus, say, 30 per cent of loans, is therefore a measure of the degree to which a bank contributes permanent capital to business. The ratio of cash reserve to, say, 70 per cent of loans, measures the temporary advances. Users of business barometers watch closely the less complex ratios of: (1) cash reserve to loans, (2) investments to aggregate assets, (3) loans to aggregate assets, and (4) the sum of loans and investments to aggregate assets. The history of the first, third, and fourth ratios is shown in the accompanying charts (Figures 2 and 3), and by subtracting the third from the fourth the second can be obtained. During the war the increase of bank cash reserves in this country did not keep abreast of the expansion of loans, the result being that the ratio of cash reserves to loans decreased precipitately. The loan account developed into an unprecedented state of extension; the banks met the urgent demands for funds to finance the war and war industries; an excessive proportion of the loans was collateraled by United States securities, and did not necessarily represent contributions of working capital to industries. The percentage increase of securities, largely United States war securities, purchased by the banks rose faster than the percentage increase of either loans or aggregate assets. As the purchase of securities is from the bank's point of view in many respects equivalent to a loan to the seller, these large purchases during the war had the effect of increasing the multiple to which banks create a loan fund on the basis of cash reserve. It might be said also that the contributions of permanent capital by banks were in effect increased both absolutely and relatively. Some liquidity was given to the war loans by

Figure 2. Graphic Chart Showing Ratio of Cash Reserves to Loans of New York Clearing House Banks. Brookmire curves used in this chart.

Figure 3. (a) Graphic Chart Showing Ratio of Loans to Aggregate Assets of All Banks Reporting to Comptroller

Figure 3. (b) Graphic Chart Showing Ratio of Loans and Investments to Aggregate Assets of All Banks

Reporting to Comptroller making paper backed by war securities eligible for discount with the federal reserve banks.

To put some fraction of a bank's funds into permanent investments is altogether safe and fitting, for in emergency they can be readily converted into cash through the stock exchange. Extensive dependence of all the banks on the securities market for such conversion, however, becomes positively dangerous. In order to accomplish a sale in a tight money market, not only must securities be sacrificed at great losses but the buyers go to other banks to withdraw funds to do the buying, thus making the market still tighter and tending to precipitate a panic. Accordingly the business world takes note of the ratios of loans and investments to total resources. The banking situation of the country becomes more critical as the proportion of loans to aggregate resources increases, because such a change means an absorption of the loan fund; and it becomes even more critical as the ratio of investments to aggregate resources increases, for the additional reason that a larger proportion of banking funds is being tied up in long-term securities which are difficult to liquefy. Babson summarizes the barometrics of these ratios as follows:1 i. During a period of business depression:

(A) An Increase In The Ratio Signifies Renewed Activity. (B) A Decrease Signifies A Further Recession In Business. (C) No Change Signifies Continued Dullness.

2. During a period of improvement following a period of business depression:

(A) An Increase In The Ratio Signifies Increased Activity. (B) A Decrease Signifies A Temporary Recession. (C) No Change Calls For Special Watchfulness.

3. During a period of prosperity:

(a) An increase in the ratio signifies that fundamental conditions are becoming unsound.

(B) A Decrease Tends To Prolong The Period Of Prosperity. (C) No Change Signifies Nothing Of Importance.

1 Babson, R. W., Business Barometrics, 1918, P. 272.

4. During a period of decline following a period of prosperity:

(A) An Increase In The Ratio Signifies Further Trouble. (B) A Decrease Is The Natural Movement. (C) No Change Calls For Special Watchfulness.

Continue to:

My Books