Chapter XIX. The Present System Of Banking

Description

This section is from the book "Banks And Banking", by H. T. Easton. Also available from Amazon: Banks and Banking.

Chapter XIX. The Present System Of Banking

When we consider the old system of banking with that of the present day we find that a great change has taken place. In early times the issue of bank notes was considered the essential part of a banker's business. Nearly the whole of his profit was derived from this source. There is, however, a close connection between the issue of bank notes and the growth of deposits in the banks of this country. Any one who had notes in his possession would in course of time come to the conclusion that it is desirable to leave them with the banker for safety, and consequently would become a depositor. The issue of notes in this country has always preceded deposit banking. We have already remarked that one of the distinctive features of modern banking is that trade is now transacted by means of borrowed capital obtained from the bankers.

It was desirable that there should be a common form for the withdrawal of money deposited in a bank. The one adopted by the banks is known by the name of a "cheque," and this, in conjunction with bills of exchange, formed the medium for transacting the modern system of credit. The circulation of cheques has largely increased in consequence of the rapid development of trade, and also has somewhat superseded the use of bank notes.

In 1844 the returns of the Clearing House were equal to 40 times the note circulation, but in 1872 these returns were equal to 135 times the note circulation.

1844 | Proportion of notes to clearing circulation = 40 | |

1868 | " " " | = 87 |

1869 | " " " | .= 90 |

1870 | " " " | = 97 |

1871 | " " " | = 113 |

1872 | " " " | = 135 |

It is important to recognise the great economy of capital which has been effected by the development of banking. The use of cheques has to some extent diminished the metallic circulation, and the system of transfers between bankers and the establishment of the Clearing House have also economised the use of gold and notes.

Mr. Jevons * gives the following account of the Clearing House system: "To obtain a clear view of the way in which bankers help us to avoid the use of money, we must follow up the rise of the system from the simplest case to the complete development of the complex organisation now existing in the United Kingdom".

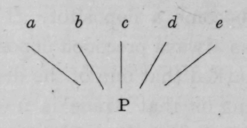

The system of one bank would be as follows: -

Let P represent the banker and a, b, c, d, e his customers. Payments are made by one customer to the other by simply debiting and crediting. If a owes b money a's account is debited and b's credited.

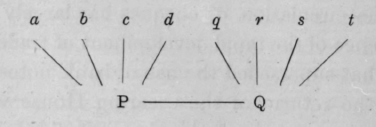

The system of two banks would be as follows: -

* Money and the Mechanism of Exchange.

Let P and Q be two bankers in a town, a, b, c, d being customers of P, and q, r, s, t customers of Q. Now the mutual transactions of a, b, c, d will as before be balanced off in the books of P, and similarly with the customers of Q. But if a has to make a payment to q the operation becomes more complex. He draws a cheque upon P and hands it to q. Not wanting coin he carries the cheque to his own banker Q and pays it into his account. There will be other persons in the town having to make payments in the same manner, and the probability is very great that some of these will result in giving P cheques on Q and some in giving Q cheques on P. The two bankers will then balance their mutual indebtedness by a single transaction.

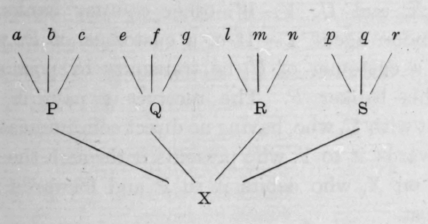

In a town with several banks the system is still more complex. The several banks need only to agree to appoint as it were a bankers' bank to hold a portion of the cash of each bank, and then the mutual indebtedness may be balanced off just as when a bank acts for individuals.

This is the system of the Clearing House. The bankers' bank is the Bank of England, but the accountant's part of the work is carried out at the Clearing House.

Let P, Q, B, and 8 = four banks, each with its own body of customers, and X = the Clearing House. P need not now send a clerk to present bundles of cheques upon Q, B, and S, but can pay them into the Clearing House, and by a system of balances their mutual indebtedness can be discharged. The balance is paid by a transfer in the books of the Bank of England.

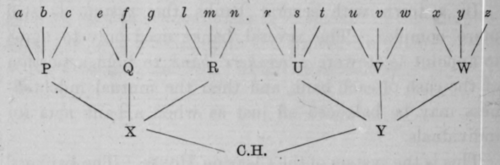

Only one further step is required to complete the system of connections between each bank in the kingdom and all other banks. Each country bank has a running account with some city bank, and all the city banks daily settle transactions with each other through the Clearing House. It follows that a payment from any part of the country to any other part can be accomplished through London.

Clearing House Let P, Q, B be country banks, having the London agent X, and U, V, W, other country banks, having the London agent Y. If a, a customer of P, wishes to pay r, a customer of U, he transmits by post a cheque upon his banker P. The receiver r pays it into his account with U, who, having no direct communication with P, forwards it to Y, who presents it through the Clearing House on X, who debits it to P and forwards it by the next post.

This system of country clearing was instituted in 1859, chiefly through the exertions of Sir John Lubbock.

In consequence of the new system about £5,000,000 of gold currency was not required for the purpose of circulation.

The Clearing House was first started about the year 1775, when a few of the city bankers hired a room where the clerks from each bank could meet to exchange their bills and notes, and the differences were then settled by money.

The joint-stock banks were not admitted until the year 1854, but all the metropolitan banks in London are not, however, represented at the Clearing House. The Bank of England does not pay its own cheques through the medium of the Clearing House, although it presents all cheques on clearing bankers. The west-end bankers and the various branch banks of the metropolis use the Clearing House indirectly by giving cheques drawn on a clearing banker.

There are three daily clearings, viz.: 1st, at 10.30 a.m. for bills; 2nd, at 12 noon for country cheques; and 3rd, at 2.30 p.m. for bills and cheques.

In the year 1839 the average daily transactions amounted to £3,000,000. The balances were then settled by the use of £200,000 in bank notes and coin, to the amount of £20. The use of notes and gold is now entirely abolished, and the daily balances are settled by transfers on the Bank of England - each banker keeping an account with that institution.

The following table shows the increase in the transactions at the Clearing House: -

£ | |

1868 | = 3,425,000,000 |

1870 | = 3,914,000,000 |

1875 | = 5,685,000,000 |

1880 | = 5,794,000,000 |

1885 | = 5,511,000,000 |

1890 | = 7,801,000,000 |

1894 | = 6,337,000,000 |

The returns for the 4th of the month show to some extent the bill transactions of the country: -

£ | |

1868 | = 155,068,000 |

1870 | = 176,137,000 |

1875 | = 245,810,000 |

1880 | = 236,809,000 |

1885 | = 221,873,000 |

1890 | = 289,107,000 |

1894 | = 261,501,000 |

In Edinburgh and Dublin the representatives of each bank meet for the purpose of exchanging their notes, upon the same principle as the London Clearing House.

There are provincial clearing houses established at Birmingham, Leicester, Liverpool, Manchester and New-castle-on-Tyne. The amount cleared at such places in 1895 was £374,856,000.

Continue to:

My Books