Collections. Part 4

Description

This section is from the book "Money, Banking, And Finance", by Albert S. Bolles. Also available from Amazon: American Finance With Chapters On Money And Banking.

Collections. Part 4

9. Collections By Outside Banks

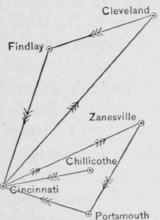

As banks, even in the large cities, do not have correspondent banks or bankers at every place in this country, what course do they take when receiving checks for collection drawn on banks outside their sphere of correspondents? Suppose a New York bank should receive a check on a bank in North Lewisburg, a small place not far from Cincinnati, what disposition would be made of the check? Obviously, the New York bank would send it to its Cincinnati correspondent, supposing it had an account with the Lewisburg bank. The Cincinnati bank might not have an account with it, and the check might go through several banks before reaching the drawee bank. The actual travels of such a check may be given to illustrate more perfectly what not infrequently happens. This check was drawn on a bank located at Chillicothe, and deposited in a Cincinnati bank. As the Cincinnati bank had no correspondent with a bank at Chillicothe, the check was sent to Zanesville, thence to Portsmouth, thence back to Cincinnati, thence to Cleveland, Find-lay, and back to Cincinnati. The third time it was sent directly to Chillicothe. In thus traveling around the state time is consumed, and it may be that the drawee bank has failed before the check is presented, whereas there was ample time for the Cincinnati bank, after receiving the check, to send it by mail or express and collect the money. In this case had the drawee bank failed, would the Cincinnati bank have been guilty of negligence in not making a direct presentation? This question was considered among bankers for several years before the question reached the courts. At last it was decided that a collecting bank was negligent when not making a direct presentation and responsible for the resulting loss. The question first arose in Nebraska. It was admitted that if the check in controversy had been presented through the agency of the mail or by express, as soon as received, there was ample time to collect the amount before the failure of the drawee bank.

10. Presenting Checks Directly

We have said that the collecting bank ought to have made a direct presentation. This remark needs qualifying. In a few states the courts hold that it is an improper thing for a bank to present through the mail a check to the bank on which it is drawn. It is asserted that the holder of a note would not think of sending it by mail to the maker for payment, as he might destroy the obligation and thus obliterate all evidence of his indebtedness to the holder. The analogy is incorrect, for the drawee bank would gain nothing by destroying the check. Its indebtedness would be just as great as before. Furthermore, there is no reason for supposing that a bank is not just as willing to pay the holder of checks the drawer's money as to pay the drawer himself. It is a matter of the utmost indifference to the bank From the point of view we are now looking at this question, the bank is the mere custodian of the depositor's money, and is just as willing to pay one person as another; it simply wishes to he sure of having adequate authority to pay; having this, it cares not in the least who the demander may be.

It has been judicially declared in one of the states denying to banks existing therein the right to make a direct presentation of checks to the drawees, that if a depositor knows this is done by his bank and continues to deposit checks therein for collection, he will be regarded as acquiescing in the practice. This especially applies to a depositor who knows that the checks deposited by him are drawn on the only bank in the place to which they must be sent for collection.

11. What May Be Received In Payment?

Lastly, what shall a collecting bank take for the checks and notes collected? Must it always insist on receiving money, or can it safely take other checks or drafts in payment? A bank in Philadelphia sent a check deposited by a customer drawn on a bank in Mississippi for collection to the drawee for payment. It sent a draft on a New York City bank in return for the amount. Before the draft was paid, the Mississippi bank failed, and the New York bank declined to honor the draft. This is a very common practice among country banks, to send a draft drawn on a New York bank in payment of a check or other claim due to a non-resident. One of the reasons why country banks keep an account in New York is to draw against it in payment for demands of this nature that may be made on them. Now and then, however, a bank fails having an account there, and the bank holding a draft that may have been drawn by the failed bank in settlement of a check drawn on itself fails to receive the money.

In a few states the rule is, the collecting bank can receive only money unless it is instructed to do otherwise. In a far larger number of states the collecting bank which receives a draft in payment from a bank in good standing is justified by law and custom in doing so; and should the drawer fail and the draft be not paid, the collecting agent can not be held responsible. This rule, which has the sanction of long custom, ought to prevail everywhere.

Continue to:

My Books