Bank Failures During Mr. Ridgely's Administration. Continued

Description

This section is from the book "The Romance And Tragedy Of Banking", by Thomas P. Kane. Also available from Amazon: The Romance & Tragedy of Banking.

Bank Failures During Mr. Ridgely's Administration. Continued

About this time the bank was due for examination and the examiner was likely to drop in any day. The president was anxious to conceal from the examiner the large unlawful loan to Mrs. Chadwick, and conferred with her in regard to making some arrangement that would pass the inspection of the examiner. The resourcefulness of Mrs. Chadwick was equal to the emergency. She enlisted the interest of some of her friends, who arranged to negotiate a loan through a trust company, but the board of directors of the company refused to make the loan when the application was brought to their attention.

The regular examination of the bank was made in April, 1904. The loan to Mrs. Chadwick then amounted to two hundred and twenty thousand dollars, and was so reported by the examiner to the Comptroller, but the examiner reported that while the loan was largely in excess of the legal limit it was amply secured and that there was no danger of the bank sustaining any loss thereon; that he had seen the security, and that it fully protected the loan. He reported this loan as having been made to C. A. Chadwick, but did not report that C. A. Chadwick was a woman, or that the security for the loan was a note of Andrew Carnegie. He assured the Comptroller that arrangements were being made to immediately reduce the loan to the legal limit and that he had insisted upon this being done.

Had this examiner advised the Comptroller that the recipient of this large loan was a woman and that the security consisted of a note of Andrew Carnegie, the Comptroller would have been put on his inquiry in regard to this woman and why Andrew Carnegie had executed his note to her for such a large sum of money, as Mr. Carnegie was not in the habit of having his notes in national banks.

At the time of the previous examination of this bank the loan was concealed from the examiner by a temporary loan negotiated by the president which was paid immediately after the examination.

In the meantime, while the president of the bank seems to have become alarmed over this large liability and appears to have made strenuous efforts to secure the payment or reduction of the loan, he continued to make further advances and when the bank failed Mrs. Chadwick was liable to the association for two hundred and fifty thousand dollars, or over four times the amount of the capital stock of the association.

The credulous president of the bank apparently was completely hypnotized by this woman and not only freely loaned to her the funds of the institution but made her liberal advances from his personal resources. So complete was his confidence in her honesty and her financial ability to fully discharge her obligations to the bank and to himself that for several days after the bank failed he still believed and maintained that she would come forward and meet her obligations.

After the failure of the association and the sensational disclosures which followed, the antecedents of this woman were thoroughly investigated and exposed, and while much that was then written of her history was no doubt untrue, or at least greatly exaggerated, according to the statements published at that time it appears that her maiden name was Elizabeth Bigley, and that she was born at or near Woodstock, Canada. She was reported to have been indicted in her younger days for forgery, but on trial was acquitted on the ground that she was mentally unsound at the time she committed the act. Later she was known as Mrs. Hoover, having married one C. L. Hoover, a resident of Cleveland, Ohio, who was many years her senior. She was next known as Madam De Vere, a clairvoyant, who formerly resided at Toledo, Ohio, and who had served a term of nine and one-half years in the Ohio penitentiary for forgery.

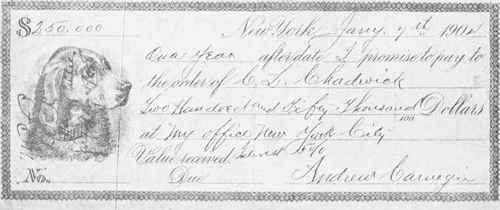

Forged Carnegie Note for $250,000.

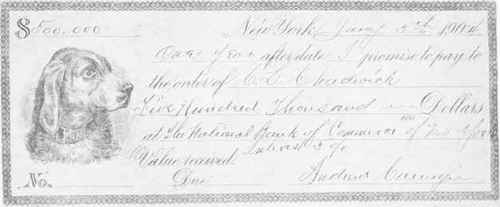

Forged Carnegie Note for $500,000, and Indorsements.

After her release from the penitentiary she is reported to have married a Dr. Chadwick, of Cleveland, and subsequently to have begun her career as a financier. Her method of operation seemed to be of the endless chain variety, borrowing from one creditor to pay another and by promptly meeting her obligations in this manner at maturity she acquired a financial standing and credit which enabled her to maintain and enlarge the scope of her operations until the end of the chain was reached in the collapse of The Citizens National Bank of Oberlin.

The reputed wealth on which she based her operations and secured credit consisted of the following so-called securities, bearing the alleged signature of Andrew Carnegie:

Two notes held by The Citizens National Bank of Oberlin for $500,000 and $250,000 respectively.

One note for $500,000.

A certificate for $5,000,000.

A certificate of trusteeship for securities held by a trust company in Cleveland for $7,500,000, making a total of $13,750,000. all of which proved to be forgeries.

At the time of her dealings with the Citizens National Bank of Oberlin, she lived at Cleveland, Ohio. Her home, it was stated, was furnished elaborately, but displayed no special taste. Her parlors were filled with carvings, statuettes and ornaments imported from Europe, and numerous paintings adorned the walls, giving the interior of her home the appearance of wealth, but the furnishings appear to have been selected without discrimination or any definite plan of arrangement.

After the failure of the bank she was indicted, tried at Cleveland and convicted for defrauding the institution and was sentenced for a term of years to the same penitentiary in which Madam De Vere had been confined years before, where she died while serving sentence.

Thus closed the career of probably the most notorious and successful bank swindler known in the annals of the national banking system.

The deluded president of the wrecked bank died before Mrs. Chadwick's trial and conviction, a victim of his own folly, caught in the meshes spread for him through his violation of the banking laws and the sacred obligation of his oath of office. The first false step in his dealings with Mrs. Chadwick was in making the original loan of thirteen thousand dollars, which was seven thousand dollars in excess of the legal limit. Each succeeding increase of credit was extended in an effort to secure and recover the previous loan, until the aggregate of her liabilities reached a point where the bank and himself individually became hopelessly involved, and the inevitable result followed.

How many bankers who have read the story of this failure and the causes which led to it, will profit by the lesson it teaches? Every president, and every cashier who is a director of a national bank, is required by law to take and subscribe to an oath that he will not knowingly violate or willingly permit to be violated any of the provisions of the national banking laws. The president of The Citizens National Bank of Oberlin subscribed to this oath and his violation of it brought disaster upon his institution, loss to his depositors and stockholders, and financial ruin and dishonor to himself.

There are presidents and cashiers of national banks who, while scrupulously honest in all their business dealings with their fellow men and religiously true to every trust reposed in them, deliberately violate their oaths of office with apparently no more compunction of conscience than had the president of the Oberlin bank. How such men reconcile themselves with their consciences it is difficult to imagine.

Bank failures that have not been due to violations of law are very rare, and if every officer and director of a bank should be true to his oath of office, temporary suspensions occasionally might become necessary under extraordinary conditions, but insolvency would not intervene, and the creditors and stockholders would not suffer loss. Because, if the officers and directors of the bank restrict the loans to any one individual or interest to the limit fixed by law, and do not undertake to circumvent its restrictions by indirect methods, the loss upon any single loan would not be sufficient to seriously affect the bank or impair its solvency. It is the excessive loan, no matter in what form it may be made, that does the damage, and no officer or director can make such a loan, directly or indirectly, without violating his oath of office and inviting the consequences that follow.

Continue to:

My Books