English Banking. Bank Of England; Peel's Act, 1844; One Reserve; Banking. And Issue Departments. Continued

Description

This section is from the "Commerce and Finance" book, by O. M. Powers. Amazon: Commerce and Finance.

English Banking. Bank Of England; Peel's Act, 1844; One Reserve; Banking. And Issue Departments. Continued

Thus matters progressed until the accession of Sir Robert Peel to the Premiership of England, and the question of the renewal of the bank's charter in 1844. The panics of 1811 and 1825, and the panicky conditions in 1837 and 1839, had aroused much discussion, and public opinion was disposed to regard the vicious note circulation which had extended rapidly and widely as the cause of these repeated commercial crises. Prior to the act of 1844 the law made no distinction in the bank's liabilities, the resources being held equally as security for deposits and the redemption of circulating notes. Under this state of affairs, if the depositors demanded coin to such an extent as to exhaust the reserve there would he no coin left for the note holders, or vice versa. In the panic of 1825 the demands of depositors reduced the reserve to only a little more than a million pounds, while there was yet outstanding note issues amounting to over twenty-three million pounds. By the act of 1844 Parliament undertook to make the notes of the Bank of England secure and limit the issue of bank notes of all other banks in the realm. With a stable currency redeemable in gold, Sir Robert Peel believed that fear and distrust, the bases of panics, would be banished from English commerce, and panics would cease, and yet three years after the passage of the act (1847) the country experienced a panic, and ten years thereafter (1857) one of the greatest financial panics ever known shook the English banking and commercial world from center to circumference, to be followed in 1866 by still a third panic of intense severity.

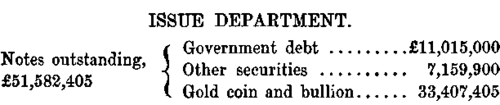

By the act of 1844 the bank was divided into two departments, viz., the banking department and the issue department. The former was to perform the functions of ordinary banking, such as receiving deposits, discounting paper, selling or buying exchange, etc. The latter was charged with the exclusive issue and redemption of circulating notes. These two departments of the bank were to be kept as separate and distinct as though they were two independent corporations. The issue department was required to hold either government securities or coin or bullion for all notes issued by it, and since the original provision limits the amount of the securities to £14,000,000, it follows that all notes issued above that amount must have an equivalent of coin or bullion in the vaults of the Bank. Of the £14,000,000 in securities £11,-015,100 due by the British government formed a part. The act also provided that the Bank might hold silver to the extent of one-quarter of its gold, and issue notes against such holdings, but this was never done. By another provision of the act, should any other bank, issuing notes at the time of the passage of the act, discontinue such issue, the Issue Department of the Bank of England might increase its holdings of securities to the amount of two-thirds of the issue of said retiring bank, and issue its own notes against such securities. By this means the Bank of England will eventually become the exclusive bank of issue, for one by one the joint-stock banks discontinue their issues, and cannot resume them, the privilege passing directly to the Bank of England.

The amount of securities held by the issue department against which notes may be issued by the bank has been increased from time to time by the discontinuance of note issues by other banks, until it amounted in 1900 to £17,775,000, and the amount of notes issued against gold coin or bullion on hand amounted to £27,116,000, making a total of outstanding circulating notes £44,891,000. It will thus be seen that the issue department of the bank is simply an establishment for the exchange of notes for bullion or bullion for notes. Every Bank of England note outstanding is practically a gold certificate, since the bank has gold on hand to pay on demand every note that it has put in circulation, except the comparatively small portion of the reserve represented by the debt, and which is partially covered by the bank's surplus. These notes are a legal tender, as long as the bank is able to redeem them in gold. By thus keeping a redemption fund of gold in the bank vaults sufficient to actually redeem the notes in circulation, the element of credit is entirely taken out of the circulat-ing medium of the United Kigdom, and the note holder knows that he can get its face value in gold at any moment. This stability of the currency, it was believed by the supporters of the Peel Act, would banish all fear from the minds of note holders and prevent the hoarding of gold. Since the hoarding of money through fear partially causes panics by making loanable capital scarce, it was contended that when the motive to hoard was destroyed panics would cease.* But the panics of 1847, 1857 and 1866 were not prevented by the stability of the currency, and in fact the panic of 1866 was only allayed by the announcement that the Bank of England had authority from the government to issue notes in excess of the redemption fund on hand. On the worst day of the panic, May 11, 1866, called "Black Friday," the bank found its reserve in the Banking Department reduced to nearly £3,000,000 at the close of business. That evening the chancellor of the exchequer recommended that the bank act be suspended, and this was promptly done by the government. The announcement on the following morning that the Bank of England had authority to issue notes beyond the limit to whatever extent was necessary, quieted the fears of the people, and affairs returned to their normal condition.

*Fear is not so much a cause of panics as one of its pronounced features, and the hoarding of money through fear intensifies the alarm by depleting the cash reserves in the banks, and by destroying their lending power for the time being, makes "loanable capital" (which may be actual money, and may be only bank credit) scarce.

Ordinarily the banking department has no power to borrow of the issue department. It may take notes to the issue department and exchange them for gold or vice versa, the same as outside persons, but during each of the three panics, viz., 1847, 1857 and 1866, the government suspended the bank act, and permitted the banking department to borrow notes from the issue department without depositing gold in exchange. No doubt the knowledge of the fact that this has been done in the past and will be done again in case future emergencies require it, will have a strong tendency to prevent panics in future.

This suspension of the banking act in case of panic or great emergency is the only elasticity of the English currency. At all other times there is no expansion to it whatever. Not a note can be issued without the gold is deposited in place of it, and hence the total volume of Bank of England notes in circulation in the kingdom is dependent upon the amount of gold in the vaults of the issue department of the Bank of England. Then again, the system has been criticised on account of the large amount of gold which is kept constantly locked up and idle, while it is claimed that a safe and conservative reserve could be maintained and still release several million pounds of gold now in the vaults which could be turned into circulation and productive use. The defenders of the system say that the act prevents the over-issue of notes, which would be a greater injury than the loss of the use of a portion of the gold reserve, and furthermore that the gold is the property of the holders of the bank notes, who have accepted the notes on condition that they could return them to the bank and receive gold for them at any time. The statement of this department of the bank May 20, 1903, was:

The suspensions of the bank act under stress of emergencies show the unsoundness of the theory or "principle" upon which it rests. Only a currency based on credit can have elasticity. Credit can both stretch and contract; money cannot, though its volume may vary both actually and relatively in any country, nor can it be made to respond automatically to the needs of the hour.

Besides the Bank of England notes there is a large amount of gold and silver in circulation in the United Kingdom, necessitated by the fact that the Bank of England does not issue notes for less than £5. The Scotch banks are allowed to issue notes for £1, and a large portion of this circulation is in small denominations.

The sources of profit of the issue department are not extensive nor numerous. The government pays 2 1/2 per cent interest on its debt (£11,015,100), and interest is received on the other securities which the bank holds. In addition to this the bank makes a profit on the purchase of foreign coin and bullion

Elasticity of the Currency brought to it, as it buys gold at the legal price of £3.17s.9d. per ounce, and turns it into the mint at a profit of l 1/2d. per ounce. The bank also derives a considerable profit from the destruction of bank bills. Any bill which is not presented at the bank counter in forty years is considered lost and credited to the profit account.

Continue to:

My Books