Indemnity For Loss By Fire. History; Classes Of Companies; Risks; Rates. Continued

Description

This section is from the "Commerce and Finance" book, by O. M. Powers. Amazon: Commerce and Finance.

Indemnity For Loss By Fire. History; Classes Of Companies; Risks; Rates. Continued

The rate, which is the prime factor in the estimation of the insurer, may be determined in either one of two ways. First, it may be made arbitrarily upon the judgment of a competent and experienced person, after a personal examination of the property to be insured. Such rates are designated "flat rates," and until recently nearly all the fire insurance rates were "flat rates." The objections to such rates were that they were not susceptible of analysis or explanation, and being made by different persons or the same person under diverse influences, they were often more or less inconsistent. Most of the fire insurance rates in late years are the products of schedules. The schedule for frame buildings is a comparatively simple one. There being no special points of construction to be considered, the schedule has reference principally to the matters of occupancy and exposure.

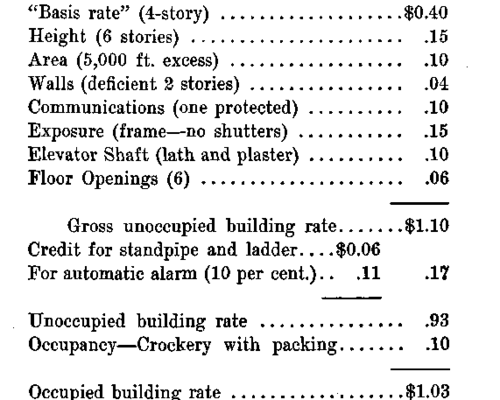

The schedule for brick buildings is a more complicated affair. In this case there is a basis rate for a standard building not over a stated height and specified ground area. The figure set for this standard building is known as the "basis rate," and it is intended to measure the sufficiency of the local water supply and fire protection, together with other conditions calculated to affect the general fire risk of the locality. To this basis rate is added charges (made according to carefully prepared tables compiled from the best obtainable experience) for the following items entering into the fire risk. The items here given are from the schedule for brick mercantile buildings of ordinary construction in use at present in the City of Chicago, Illinois.

1st. Height. For each story over the standard height, a charge is made; this charge increases with the stories, because the difficulty of reaching and extinguishing a fire increases in proportion to the height of a building.

2d. Area. The risk of spreading fire increases directly as the area of the building and a charge is made for area, over standard, accordingly.

3d. Walls. To protect the building from adjoining buildings and to bear the weight of its contents, a building should have walls of certain strength, and deficiency in that respect is charged for in the schedule.

4th. Communications. An opening into an adjoining building makes possible the communication of a fire. If the communications are unprotected, the buildings are rated as one risk. If the communications are protected by proper iron doors, there is a charge made on the theory that the doors may not be shut in case of fire; this charge increases with the number of such communications.

5th. Exposures. Charge is made for exposure based upon the seriousness of such exposure, its nearness and the precautions taken to guard against the exposure.

6th. Elevator shafts. Unless built of non-combustible material with fire-proof doors at each floor, an elevator shaft acts as a flue to carry a fire to every floor in the building, and is heavily charged for under such circumstances.

7th. Floor openings. Stairs and other minor floor openings act much as an elevator shaft, though in less degree, and they are charged for accordingly.

8th. Condition. It is becoming more and more the practice in schedule rates to charge for unsafe condition of premises. These charges are intended to be temporary in their nature, and are supposed to measure the hazard existing by reason of poor condition of premises. As soon as the premises are put in safe condition the charge is removed. By reason of careless management, however, charges for condition often amount to a permanent charge, and become an unnecessary tax on the business.

Credits are allowed for protection intended to prevent the inception or the spread of a fire. Stand pipes with ladders on buildings, giving assistance to firemen, are the basis for a credit of one cent for each story. Automatic fire alarm service, or telephone watch service reporting to a central station is a large measure of protection, and for these a credit of ten per cent of the building rate is ordinarily allowed. Special construction, such as open mill construction, and other superior construction, is encouraged by an allowance in the rate. Automatic sprinklers (a system of piping through a building with faucets which are opened by the melting of a fusible link, back of which are adequate water supplies in gravity or pressure tanks), afford the best protection known at this time against the spread of fire, and for this system of protection a very considerable credit is allowed in the insurance rate.

There are other charges and credits, but the ones cited will suffice to explain the theory on which the unoccupied building rate is constructed in the process of schedule rating. After the unoccupied building rate is ascertained, a charge is made for the occupancy, according to the hazard of such occupancy, and the result is the rate

Credits

Building Rate at which the building insurance is written. Applying these principles for an example, we might find such a case as this:

Having ascertained the rate on the building (which in this case is made more than ordinarily complex, for the purpose of illustration) the next step is to calculate the rate on the contents. On the theory that any brick building is better than its contents, there is added to the occupied building rate a certain sum intended to measure the susceptibility of the contents to damage by fire or water. For example: Boots and shoes in cases would classify twenty-five cents more than the building. An open stock of dry goods, 50 cents; a millinery stock, 80 cents, and a stock of tobacco, $1.00. Taking the crockery stock, for example, there would be added to $1.03 (the occupied building rate) 45 cents for a crockery stock, making the rate on the contents, $1.48 per $100 of insurance per annum.

If there is more than one tenant in the building, on the theory that each additional occupant introduces some moral and physical hazard, there is a charge made, the amount of which charge is determined by the nature of the occupation. If a stock of merchandise occupies but one floor in a building, it is charged for location. The grade floor is standard, with no charge for location. In the basement, ten cents are added for liability to water damage, while above the first floor, the "loading"* for each floor is the square of the floor occupied. For example the loading for the second floor is four cents, the third floor nine cents and so on. The loading for stocks occupying more than one floor is obtained by striking an average for the floors occupied. When the entire building is occupied by a single concern no floor loading is made.

For buildings of fire-proof construction there is a "fire-proof schedule," designed to meet the different and complex conditions found in this important class of risks. Likewise for manufacturing risks, there are special schedules intended to measure the hazards existing in the different processes of manufacture with credits for safeguards calculated to eliminate or reduce such hazards.

•Loading is a term used for additions to the basis rate on account of location or other special conditions.

Continue to:

My Books