Capitalization Of Monetary Incomes. Part 2

Description

This section is from the "Economics In Two Volumes: Volume I. Economic Principles" book, by Frank A. Fetter. Also available from Amazon: Economic

Capitalization Of Monetary Incomes. Part 2

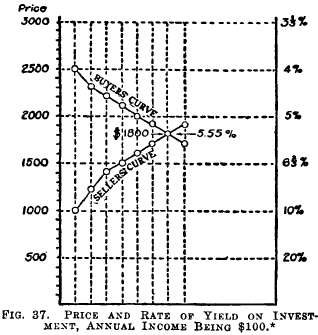

§ 4. Price and rate of income. It may be shown by a price diagram how every price arithmetically involves a corresponding rate of premium on the present price (investment of capital) which will be unfolded as an income to the investor. Take the case of a house affording a net rent to the owner of $100 a year (after allowing for taxes, costs, depreciation). The price of the series of incomes is the amount at which the bids are brought to equilibrium, the marginal bidders being those just ready to drop out of the market if a slight change is made. This reflects the rate of time-preference in the individual economy, showing itself in the whole state of improvement and depreciation of agents in the possession of each man. B will prefer to rent so long as the house is priced at $2000 (involving a rate of 5 per cent) but prefers tc buy when it is priced at $1800, a discount of 5.55 per cent. The expression of the price of time as a percentage is merely a convenience.

§ 5. Bonds and mortgages as saleable incomes. The modern corporation bond is a promise to pay an annual sum, expressed as a percentage of the principal, and to repay the principal at the definite date of maturity. A twenty year 5 per cent bond for $1000 thus is a promise to pay 19 annual incomes of $50 at the end of each year (but see note below) and one payment of $1050 at the end of the twentieth year. It could as well be termed a 20 payment $50 a year bond with a maturing value of $1000, without mentioning a rate of interest. The rate it truly yields the investor depends on the price he pays, which is fixed by market conditions. Such a bond does not necessarily sell at par (its denomination); usually it sells at a premium or at a discount. The investors treat a bond as so many incomes distributed at certain points of time, and bidding in the market fixes the market-price for future incomes of that type.2 A note secured by real-estate mortgage is like the bond, but not so marketable, and is ordinarily held by the same investor until maturity. It usually (but not always) is bought at its face value and the holder looks upon it as capital to that amount. But as it is not payable until the date named as maturity, he could, if he wished, convert it into ready funds before it is due, selling it at the best price he can get, which may be above or below par. Thus a ten year mortgage for $5000, bearing 5 per cent interest, may be looked upon as containing nine annual payments of $250 each and a tenth payment of $5250. The total undis-counted sum of all the payments is $7500; and if the mortgage is bought at par it yields an annual net income of 5 per cent on the investment; if bought above par it yields an income of less than 5 per cent (e.g., bought at $5406 it yields 4 per cent).

* This shows graphically that, the net yield of a durative agent being given, every possible price (capitalization) arithmetically corresponds with and involves a rate, which evolves as a rate of income on the investment.

2 In most cases the interest on bonds is payable semi-annually (at the end of each six months) and the bond tables showing the "rate of interest realized if purchased at prices named and held to maturity," otherwise known as the investment yield, are usually prepared with this condition in mind. This is equivalent to a slightly higher rate of interest.

This is a good illustration of what is meant by capital as contrasted with wealth. If the mortgaged house will bring a price of $10,000, that is the price of the wealth; but the owner has a capital of $5000, and the holder of the mortgage has a capital of $5000-which together are the total value of the wealth.

§ 6. Price of variable and terminable incomes. Cases of entirely uniform and perpetual incomes (even in expectation) are very rare. Most incomes are variable and terminable. These are capitalized and made comparable as to present worth with a uniform and perpetual series. Incomes may change in an upward direction, more or less regularly from year to year; they may decrease or they may remain the same for a series of years and then terminate abruptly; or they may vary by any combination of these changes.

Especially in modern times real-estate rentals, formerly the type of stability, have been rapidly altered by social changes, and so far as these changes are foreseen, expected rents are made the basis for present capitalization. Investors and owners alike may foresee that a piece of land used only for agriculture will, within a few years, be taken up for city lots, or will be needed for a factory or as the site of a railroad station. A vacant lot may be held for a number of years at a good price while yielding nothing; in this case the incomes are all future, and the capitalization must be based upon the progressive series expected, beginning at zero. In some cases the physical output of any agent may decline while the price of the product increases, the resultant being perhaps a stationary yield or an increasing one. When foresters foresee that the selling price of the timber will be greater twenty-five years later than it is to-day, and they estimate the future yield of the forest on this basis, they advise expenditure that would be unwise if present prices were to continue. Again when the expected series of incomes is declining, as the royalties secured from mines, being certain to disappear at some more or less calculable date, the capital value of the mine is the present worth of a limited and degressive series of incomes.

The value of a short series may be calculated by simple arithmetical methods, and more easily by the aid of a table of present worth, when any rate of premium on the present is assumed. Suppose the rate to be .05 and the incomes expected are as follows: at the end of the 1st year, 100, of the 2nd year 75, of the 3d year 50, then ceasing. The present worth is the

Again it must be observed (see Chapter 22, sections 8, 9) that if the price is $206.46 it mathematically involves the rate of 5 per cent, quite independent of any thought; the calculation merely reveals and expresses exactly a rate inherent in the transaction. § 7. Depreciation funds. As a matter of practice the more difficult calculations of variable and terminable annuities are avoided by investors by taking the perpetual uniform series of incomes as the standard with which all the other series may be made comparable. They treat the original capital invested as a sum to be kept intact to be reinvested. The payments at the end of each year are treated as gross income to be divided between a depreciation fund sufficient to maintain the capital unimpaired at the end of the period, and net income which may either be spent or be saved (reinvested as an additional capital). In all bonds bought above par the amount to be treated as a depreciation fund is larger in proportion to the nearness of the maturity of the bond, and in turn, the more distant the date of maturity the higher the present price of a bond bought or sold above par.3 This method of calculating the capital investment as equivalent to a fixed sum of money is convenient, especially in distinguishing between income and principal. When losses are great they fall upon capital, and the income is a negative quantity. "When prices of bonds rise, the income is larger than was expected, and (unless taken out in some way) is by a mere bookkeeping process counted as added to the capital, and the rate of income thereafter is reckoned on a higher basis of annual investment.4

Continue to:

My Books