Costs And Competitive Prices. Part 2

Description

This section is from the "Economics In Two Volumes: Volume I. Economic Principles" book, by Frank A. Fetter. Also available from Amazon: Economic

Costs And Competitive Prices. Part 2

§ 4. Main classes of costs. These two cases present in comparatively simple form the problem which every larger business involves in very much more difficult form. The total costs of any business are roughly distinguishable as fixed costs (or fixed charges) and variable costs. Fixed costs are those which remain unchanged on the business as a whole, or on some department, no matter what the size of the output. There are some costs, as the rent of office, factory and store, salary of manager and clerks, etc., which would go on if nothing were sold, unless the business were closed. Variable costs are those which are attributable solely and exactly to particular units of product, rising and falling exactly in proportion to the output.1 In truth, costs share these characteristics in a great many degrees, are more or less fixed or variable, and are never (or with very meager exceptions) either absolutely fixed or absolutely variable.

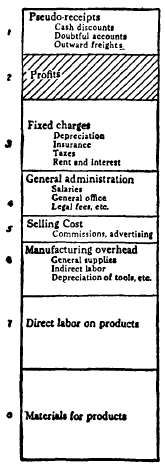

The variable costs are also called direct because put upon the particular unit of goods, and the fixed costs are correspondingly called indirect, or overhead charges. It is a very difficult matter, and yet one of very great importance, to arrive at principles and practical working rules by which in each business the various elements of cost may be allocated to different departments, classes of goods, and particular units of output. For this end a special art of cost accounting has been developed, and a special class of expert cost accountants. The principal elements of costs distinguished in cost accounting are represented in Figure 46.

1 "Variable" does not mean that the unit price of the factor necessarily changes, e.g., that the wage paid per piece for making the articles varies; nor "fixed" that the unit price of these factors is unchanging. The meaning is that in the one case more are needed, and in the other the amount needed remains unchanged, regardless of the size of the output.

Fig. 46. Elements of cost. This figure may be taken to represent either the total costs of a year's business or the costs of a particular unit of goods. In the first sense the whole rectangle represents the total receipts from sales. Of these, the part marked 1 represents deductions from sales which are pseudo-receipts (mere bookkeeping items) and might be first deducted, leaving the rest of the column to be distributed among costs and profits. (See items below.) Some of these items are differently classified by cost accountants. "Cash discount," allowed to customers for prompt payment of bills is, perhaps for convenience rather than logic, included by some in fixed charges. "Doubtful accounts" is, together with "depreciation on plant" (see fixed charges), included in another general class of "reserves" set aside to cover these items. "Outward freights," those paid on goods shipped to customers as a part of the agreement at sale, might perhaps more logically be counted as a selling cost. At the bottom are shown the most variable elements of costs in manufacturing, which are materials (8) and direct labor (7), the kind employed directly on the product, and which in large part can be employed and discharged as need requires. Then come the manufacturing overhead (6), which includes general factory expenses, as factory office supplies, heat, light, power, repairs, and renewals; labor, indirect, such as foremen, porters, cleaners, messengers, watchmen, teamsters; salaries of superintendent or master mechanic, and clerical help on shop accounts (as distinct from the work of the general administration or of the selling department) ; and depreciation of tools and machinery as distinct from the general plant.

Then come (5) selling cost, the main items of which are salesmen's salaries and commissions, and advertising; (4) general administration, which includes salaries of the officers, and fees to directors, and general office expense, traveling, printing and stationery (not advertising), postage, telephone and telegraph, legal retainers and fees; (3) fixed charges, which include depreciation (if not put into a special reserve), insurance on the plant (which as a safeguard against fire, is a substitute for depreciation), taxes, and finally rent and interest. These items may cover either actual rents and interest paid, or hypothetical rent and interest, the normal amount of income on a passive investment of the same estimated value. The remainder at the close of the year, as indicated in the shaded space, is profits in a wider or narrower sense, according as it does or does not include the amount normally attributable to a passive investment.

§ 5. The problem of cost accounting. The difficult task of cost accounting is to break up this annual total into minute fractions and to distribute them in due proportion so as to tell if need be the cost and profit on any unit of product. Sometimes a large undertaking turns out a single, homogeneous physical product, as gas, electricity, water, bricks, salt, paper of a certain grade, spools, pig iron, etc. Here a unit cost and profit can easily be estimated from the total annual figures; but if the management desires to ascertain the cost of each of the series of processes through which each unit goes, the problem becomes more complex. Another type of undertaking makes numerous kinds of goods, but in standard patterns, such as tools, machines, stoves, wooden furniture, carpets, cloth, etc. Here the unit cost is estimated by following the product through the various departments, and this cost figure once fixed can be used continuously and repeatedly tested. Another type of business does all its work on special orders, such as job printing, electric installation, house contracting, etc. The constant recurrence of somewhat similar kinds of jobs tests the estimates and permits a pretty exact allowance to be made for the usual delays and losses.

§ 6. Homogeneous products with unequal costs. But no matter how carefully these unit-cost figures are worked out, the salesman is tempted repeatedly to ignore them. He sees a chance to sell below cost and still make a profit. This is the paradox of price cutting. It is an ever-besetting temptation of the business man, sometimes leading him to profits, but often to his undoing. The key to the mystery is already in our hands: it is that all costs are in some measure joint-costs, and that every estimated several-cost has something of arbitrariness in it. Take a case where this would seem to be least true, where the entire output of a large industry is a single homogeneous product, such as water, electric current, etc. Here surely, if anywhere, the unit cost is certain, being the simple arithmetic quotient of total cost divided by the number of units. But, no, as frequently here as in any business the seller finds differences of a real character and is forced to assume differences in other cases in order to make a sale. In some cases he finds the estimated cost to be incorrect, in others he finds it to be futile. The cost of reading meters, keeping up the service pipes, and rendering bills is greater per unit of water, gas, or electricity, for small users than for larger ones. This can be adjusted by making a flat fixed charge to each consumer for meter and labor, little if any more for large than for small consumers, and a separate charge per unit of product alike to all. For example, if electricity is charged at 13 cents a kilowatt hour, the bills would be Customer A, using 10 kilowatts monthly @ 13 cents = $ 1.30 Customer B, using 100 kilowatts monthly® 13 cents = $13.00 If a charge of $1 a month per customer is made for meter, etc., and a separate charge of 3 cents per kilowatt hour, the bills would be Customer A, uniform charge $1.00 plus $ .30 = $1.30, actual price, 13 cents per k. h. Customer B, uniform charge $1.00 plus $3.00 = $4.00, actual price, 4 cents per k. h. § 7. Principle of charging what the traffic will bear. But where no such reasonable explanation can be found,2 and the outward conditions all point to a uniform cost, the seller is repeatedly faced with a situation where at the moment and, as he says, " for practical purposes," he is impelled to assume a difference. The business is there as "a going concern," a large part of the charges are, or appear to be, fixed charges -in any event will not be increased by the particular increase of product in question, which will more fully and proportionally utilize certain parts of the equipment. The new business can not be secured at the average rate paid by a similar class of customers (possibly because of this customer's advantageous position to buy somewhere else, or because he can produce for himself more cheaply than the average customer, etc.). A lower rate is made to get the new business, while the old customers continue to pay the old rates, the result being that the total profits of the enterprise are increased. There is scarcely an enterprise, large or small, in which essentially this situation does not sometimes present itself.

2 There are numerous other reasons for classifying customers, which must be reserved for discussion with practical problems. The example is sufficient for our present purpose of explaining the principle.

But note this: unless the price to the other customers is reduced to the new rate, there is here discrimination in prices, unlike charges to like customers, for substantially the same service. The price is on the principle of charging what the traffic will bear. A portion of the customers may be bearing all or nearly all the fixed charges, while another portion is bearing little more than the variable charges occasioned by their part of the output. By a sort of historical accident the late comers get the benefit of the economies of an established business which the early comers made possible. Altho the old customers are charged no more than they were before, they are now charged more than are other customers, possibly their competitors; and this may have practical effects quite as serious to them as if they were charged absolutely more than they were before.

Continue to:

My Books