Profits And Costs. Part 4

Description

This section is from the "Economics In Two Volumes: Volume I. Economic Principles" book, by Frank A. Fetter. Also available from Amazon: Economic

Profits And Costs. Part 4

§ 10. The genealogy of value. When the one factor yields several different kinds of products no one product alone accounts for the value of the factor. As any one wishing the factor for any use must bid against the other uses, the factor appears, on a superficial view, to have a price already determined by its other uses. But we know from our previous studies (see Chapters 4-6) that the value in any situation results from all the uses taken together, including the particular use we began to examine. To take a simple illustration : a savage finds in a wreck on the coast a number of bars of iron. He and his fellow tribesmen wish them for various purposes: to make arrow heads, spears, knives, hatchets, hoes, ornaments, nails, needles, etc. The value of a bar used to make a knife is in this case derived, in part, through the ultimate factor, from the alternate uses. Taken jointly and considered as one sum, the values of the products account as completely and exclusively for the value of the factor as if they were merged into one product. The factor (F) is distributed to each of the products in accordance with the marginal principle and therefore the value of the various products from equal quantities of any factor constantly tends to equality. Any unit of product sought for any purpose must be paid for according to a value determined by the costs of the factors under the marginal rule in all the applications. The genesis of the value of ultimate factors is found in the value of the product.

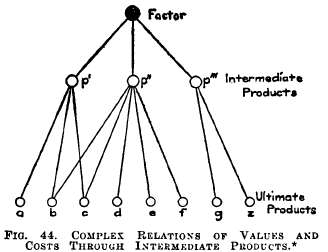

* A factor F (it may be a concert singer, an acre of land, or a mineral spring) derives its entire value (usance and capital value) from the price of the product, is valuable or worthless according as the product is so. If two or more products (p', p", p'") are attributable to it, its value is the sum of their prices (less costs, that is, the prices paid for other factors). But inasmuch as the use of F for one product takes it away from the use of another, the value of its use must be accounted as a cost whenever it is a question of increasing the output of any one of the products. Therefore, at that moment the cost seems primary and price derived.

* The figure shows how the value of a unit of product at a is reflected up to the source, and through successive links to the most distant product z. The effect of this is to reduce the sale of z and correspondingly the use made of the agent in question. A higher price of leather, p", due to the increased use of shoes (f), raises the value of hides and cattle (F) and raises thus the cost of carriage-trimmings, pocket-books, footballs, leather belts, and every other leather product (b, c, d, e). As the price rises, substitutes for leather, and imitations of it, are used for such of the products as can not bear the increased cost of leather. As more cattle are raised to provide the leather, the value of meat (p'") falls, and likewise soap (g) and oleomargarine (z).

In actual life the problem is far more complex, and yet, through its settlement runs just the same principle. There is constant bidding for factors, and through their prices the claims of rival products are adjusted. A point is reached where it does not pay to use any more of an agent in a certain industry; the production of another unit results in a loss because the factors are worth more in other uses. There is a most complex relation among many different industries using the same factors. Thus in countless ways the values of products of widely different kinds mutually influence each other. The value of no one is an isolated fact, but is ultimately only the reflection of its relative importance in meeting the desires of men in view of the whole situation.

§ 11. Money cost derived from price of products. Products compete with each other for the factors that enter into them. According to location, quality of the soil, and improvements, a certain area of land has various rival uses. These uses bid for the land; that is, put in an economic claim for it. Products of a higher value outbid and exclude those of a lower. If fine wine can be raised on a piece of land, potatoes ordinarily will not be planted in it. But if there is such a supply of that quality of land that it continues to be used side by side for both products, it will have the same value and yield the same rental in both uses. The law of indifference applies. The demand for any factor entering into products is reflected, in an increased price, to its cost in all competing products. Machines are usually made for some product determined in advance, but often they are only partially specialized and within limits they can be adapted. Sewing-machine factories were readily turned to the making of bicycles at the time of greatest demand, and bicycle factories later were used for the making of automobiles. Thus, in general, machinery is used for the product in which it can realize its highest value. Any enterprise seeking it for any other use finds its "cost" affected by its various alternative uses. The same is true of all the materials and of all the grades of labor entering into products. The enterpriser's cost is therefore the reflection of the ultimate prices of the productive agents in all its other uses as well as in the particular product he desires.

§12. Cost an expression of consumers' estimates. We thus conclude that even where cost appears to be the limiting influence in the price of a particular product, the cost is itself fixed by a larger group of influences, the demand for the factor in the totality of its uses. Wherever cost asserts itself the enterpriser must bow to the situation, and must conform closely to costs or suffer a loss. The consumer by deciding to buy this or that product sets into motion waves of value. The enterpriser transmits these to the factors. He is the medium through which consumers express their estimates. The enterpriser who anticipates aright and satisfies the public taste is the good medium. He readily transmits and accurately focuses the rays of public judgment. The enterpriser who misjudges is a poor medium. The one realizes profits, the other incurs a loss.

Notes

On other meanings of profit. It is well to note for caution's sake other loose uses of profit as any gain or advantage secured by any means in business. In retail business it has the meaning of the gross gain on a given sale, the excess of the selling price over the price at which the merchant bought it from manufacturer or wholesaler. Let us call this sale-profit. Buying an article for one dollar and selling it for two dollars, is said by the merchant to be selling at 100 per cent profit, jocularly called, "The Dutchman's one per cent." In different lines of goods there is added regularly to this cost 20, 30, or 50 per cent, as the case may be, as the merchant's profit on the sale. Sale-profit leaves out of account rent, interest on capital, clerk hire, freight, and many other minor items that enter into the cost of running a store. It often happens that the Dutchman's way of reckoning is near the truth, and that the sale-profit of 100 per cent leaves at the end of the year hardly 1 per cent of the sales as a true income to the merchant. This meaning is sometimes developed to a yearly sales-profit, the sum of all the separate sale-profits within a year, or the difference between the wholesale and retail prices of goods sold within the year.

Another meaning is given to the term by expressing yearly sales-profits as a percentage of the capital invested. The rate of profit in this case varies partly with the rate of the turnover. To illustrate: if the amount invested in a printing-office is $100,000, and the annual business done is $300,000, the capital is said to be turned over three times; if the yearly sales-profit were 20 per cent, the ratio of sales-profit to investment would be 60 per cent; but, if the capital had been turned over four times, the rate would have been 80 per cent on the investment. In none of these cases is profit used truly as an income.

The source and cause of profits in economic writings. Profits, as used by the English economists from Adam Smith ("Wealth of Nations," 1776) to John Stuart Mill ("Principles of Political Economy," 1848) and after, was the residual amount combining the incomes attributable to the personal management together with the capital-investment. These functions were assumed without discussion to be united in one person, as they usually were, stock companies at that time being rare outside of banking and foreign trading companies. The capital-income was assumed to be much the larger part and there was almost no thought of the varying degrees of ability in management as affecting the result. Hence profits in the older English economics often means nearly the same as yield from capital, peculiarly the income of the capitalist; tho usually it means this plus an allowance for risk and services of management. "Normal" profit was thought of as varying from one class of business to another but not very clearly as varying from one establishment to another.

Then the pendulum swung in the other direction and some writers, notably the American, Francis A. Walker, made profit mean almost solely the earnings of management, it being assumed that financial resources naturally rolled into the possession of able business managers. But, as it was assumed that they always had some capital themselves, the concept of profit still had a dual character. Capitalists were thought of as always getting a contractual income, interest, whereas the entrepreneur got an income varying from zero (or a minus quantity) upwards, according to his skill in management.

Continue to:

My Books