Sec. II. Cost Of Production From The Economist's Standpoint

Description

This section is from the book "The Principles Of Economics With Applications To Practical Problems", by Frank A. Fetter. Also available from Amazon: The Principles of Economics, With Applications to Practical Problem.

Sec. II. Cost Of Production From The Economist's Standpoint

1. The economist should view money cost as an intermediate and not as an ultimate explanation of value. The value of all things must be traeed back to gratification, to the relation of goods with psychic income. This being true, the value of the factors which the enterpriser uses must be derived from the value of the products, and not the reverse. This does not mean that the business man is deceived into the belief that he has in cost of production a final explanation of value. He simply is not interested in that question. He knows that there are many influences determining the cost of the factors he buys, but they are distant; he cannot influence them, and in the single stage of his production they seem to fix the price. In some purchases, and on the stock exchange, a marvelous recognition and analysis of the most distant influences is necessary; but in general a superficial view of value is taken in business; it does not pay to do other. The logical treatment, however, must go deeper into the question and trace the cost of agents back to the ultimate cause of value, that is, to want-gratifying power. To say that the price of a product is determined by the money cost, or price, of the factors is simply to postpone the answer to the question of value; one has still to ask, What determines the money cost, or price, of those factors themselves?

Money cost not the ultimate explanation of value.

2. The demand for any factor entering into products is reflected, in an increased price, to its cost in all competing products. Figuratively speaking, products compete with each other for the factors that enter into them. According to location, quality of the soil, and improvements, a certain area of land has various rival uses. These uses bid for the land, or put in an economic claim for it. Products of a higher value outbid and exclude those of a lower. If fine wine can be raised on a piece of land, potatoes ordinarily will not be planted in it. But if there is such a supply of that quality of land that it continues to be used side by side for both products, it will have the same value and yield the same rental in both uses. The least utility yielded by any portion of the supply fixes the value of all the units.

The cost of agents is fixed by their marginal utility in alternative uses.

Machines are usually made for some product determined in advance, but often they are only partially specialized and within limits they can be adapted. Sewing-machine factories were readily turned to the making of bicycles at the time of greatest demand, and bicycle factories later were used for the making of automobiles. Thus, in general, machinery is used for the product to which it contributes the most value. Any enterpriser seeking it for any other use finds its "cost" affected by its various alternative uses. The same is true of all the materials and of all the grades of labor entering into products. The enterpriser's cost is therefore the reflection of the want-gratifying power of the productive agent in all its other uses as well as in the particular product he desires. To the enterpriser, cost seems the cause of the value of a product. To the economist it should be clear that the utility found in the various products is the basis of value in the factors, i. e., of the costs.

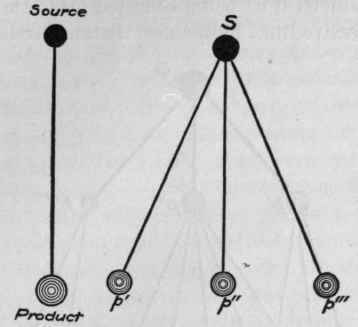

A single source of a single product.

3. The genealogy of value may thus be traced through the various intermediate products to consumption goods. A single product having a single source of supply shows most clearly the reflection of value directly from the product. The discovery of a mineral spring or of a good quality of building-stone on worthless land, will cause a value to attach at once to the source of supply. When a great singer like Adelina Patti commands several thousand dollars for each appearance in concert, the source is the magical throat of the singer, and the salary reflects the utility of the music in the minds of delighted hearers.

One source of several products.

When the one source of supply yields several different kinds of products there is just one new condition which confuses the thought and suggests the error that value begins in the source (with costs therefore) and not in the product. Looking at the products severally, no one of them explains the value of the source, and, on the contrary, each one is seen to have a value independent of the particular use to which it is put. To make the illustration most simple: a savage finds in a wreck on the coast a number of bars of iron. His fellows wish them for various purposes: to make arrow heads, spears, knives, hatchets, hoes, ornaments, nails, needles, etc. Value is in this case derived in part, through the source, from the alternate uses. Taken jointly and considered as one sum, the value of the various products accounts as completely and exclusively for the value of the source as if they were merged into one product. The source (S) is distributed to each of the products in accordance with their marginal utility, and therefore the value of the various products from any source of supply constantly tends to equality. Any unit of product sought for any purpose must be paid for according to a marginal utility determined in all the applications. The genesis of the value is in the utility of the product; the value of the source is derived.

1. A single Product 2. Several Products from one Source.

In actual life the problem is far more complex, and yet, through its settlement runs just the same principle. There is constant bidding for materials, and through their price the claims of rival products are adjusted. A point is reached where it does not pay to use any more of an agent in a certain industry; the production of another unit results in a loss. There is a most complex relation among many different industries using the same factors, the value of a unit of product (at a) being reflected up to the source, and through successive links to the most distant product (z). The effect of this is to reduce the sale (of z) and correspondingly the use made of the agent in question. A higher price of leather, due to the increased use of shoes, raises the value of hides and cattle (this increasing the extent of cattle raising) and raises thus the cost of carriage-trimmings, pocket-books, foot-balls, leather belts, and every other leather product. As the price rises, substitutes for leather, and imitations of it, are used for such of the products as cannot bear the increased cost of leather.

Complex conditions with intermediate products.

3. Complex Relations Through intermediate Products.

The enterpriser the medium of price movements.

4. The enterpriser does not fix the value of products or of agents, hut is the medium through which consumers express their estimates. The enterpriser who anticipates aright and satisfies the public taste is the good medium. He readily transmits and accurately focuses the rays of public judgment. One that misjudges is a poor medium. The enterpriser is himself the servant of costs. Laborers sometimes assume that the employer can dictate wages, prices, and markets, can rule things with a lordly hand. With rare exceptions the ultimate control in these matters by business men is very slight. In the main the enterpriser masters the situation only by bowing to it, just as the scientist and the engineer gain mastery over nature because they know when to bend and how to obey. The consumer, by deciding to buy this or that product, sets in motion waves of value. The consumers of products are the true purchasers of labor, materials, and uses of agents. The enterpriser must conform closely to cost, to the price prevailing for the moment, or his competitors in this day of narrow margins will seize the opportunity. The enterpriser is merely the distributor or equalizer of cost among all the different products for which different agents can be used. If he acts efficiently, profits arise.

Costs are an expression of consumers' estimates.

Questions On Chapter 30. Cost Of Production

1. What is the cost of a good you have made entirely with your own labor?

2. What is the difference to the employer between rent, interest, and wages as items of cost?

3. Is there anything in common between "cost, the onerous exertion necessary to get goods," and cost as the money expenses of production?

4. Why does a merchant engage in one business rather than in another?

5. When prices fall, what determines which factories shall close, and which workmen shall be discharged?

6. Does the value of a product conform to the capital that has been put into it.

Note

For a fuller treatment of the more recent view of the subject, see Smart, pp. 64-83; Wieser, Natural Value, pp. 171-214; Bohm-Bawerk, Positive Theory of Capital, pp. 179-189, 223-234. The defects of such revisions as that attempted by Alfred Marshall are pointed out in Quarterly Journal of Economics, Vol. XV, pp. 432-452, article "The Passing of the Old Rent Concept."

Continue to:

My Books