The Science Of Speculation. Economic Basis Of Speculation. Part 3

Description

This section is from the "Investment And Speculation" book, by Louis Guenther. Also see Amazon: Investment And Speculation.

The Science Of Speculation. Economic Basis Of Speculation. Part 3

Speculation In History

By no means, either, is speculation in any sense a modern force. It is as old as the human race. Only when the human race no longer exists will speculation become extinct.

Our own Bible brings down to us the tradition of how Joseph bought up all the wheat in Egypt because he shrewdly detected there would be a famine in the land. What was this but speculation? In reality Joseph was the first man we know of to corner wheat. Nowadays men speculate in the same cereal. They watch the weather map carefully and spend considerable money each year gathering statistics in an endeavor to form an idea as to the extent of the harvest. As they form their opinions they trade in the wheat long before it is out of the ground and ready for the market. They buy if they believe the crop will fall short, to resell it later at a higher market price, or if, on the other hand, they arrive at the conclusion that the crop will be plentiful, they sell it in anticipation of a decline in the price expecting to reimburse themselves from the difference in the price they agreed to deliver it for months previous to the harvest. If they are mistaken in their judgment, they, of course, are out of pocket. The only difference between their trading and that of Joseph is that whereas he bought the wheat outright, they deal in contracts without ever seeing the cereal.

Guglielmo Ferraro, the great modern Italian historian, in his fascinating history of "The Greatness and Decline of Rome," gives a very interesting account of how speculation was at the bottom of most of the conquests of the Roman legionaries over the barbaric nations, and to many it may be exceedingly interesting to know that for nearly a century before the birth of Christ, the Romans were already buying shares in large land operations which were carried on throughout the colonies of Rome. So even the buying of shares, regarded as a modern evolution, is by no means new.

Lucullus, Rome's first great expansionist, inaugurated the fashion. His conquest of Mithridates first opened the eyes of the Romans to the luxuries and refinement of the East. The talents and sesterces he brought back to Borne incited in the Roman aristocracy the lust for greater conquest. The rich money lenders were prompted to finance the expeditions and the ambitions of the Roman war lords. Pompey conquered other nations, turning over their rich lands to the powerful Italian land operators, who in turn invited the smaller speculators to join them in their extensive operations. Caesar con-tinued Rome's policy of conquest in Gaul and Britain. Behind all his wars was the sordid object of enriching himself and his followers with the tributes exacted from the smaller and weaker tribes which his legions subdued - all for one object, to extend the wealth of Borne,'to give the speculators a greater field for their operations.

Thus it is seen that we have many historical precedents to justify speculation. More than this, they indicate that behind each step of progress the human race has made speculation has been the impelling force and modern conditions have changed it but slightly.

Certainty In Speculation

What, however, is the science of speculation? We often hear of this appellation being applied to it. Roughly speaking, to me there does not seem to be anything like a science of speculation, in the ordinary sense of the term, beyond a few general though uncertain rules. There is a science of chemistry. The knowledge gained of it can be verified by exact observation. Certain conclusions can be demonstrated beyond peradventure by the exact result which an investigator sets out to obtain. There is an exact science in astronomy, in medical research, in geometry, in meteorology, and in metaphysics. Knowledge of laws and rules must first be acquired to prepare a person to undertake investigation in these sciences.

But I should like to ask how any course of study in speculation could be outlined on which reliance could be placed. Familiarity with the objects engaging one's speculative instincts is, of course, absolutely essential to success. A general knowledge of conditions helps considerably when coupled with a keen perception of their probable effects, but as these conditions constantly vary, there is no way by which a knowledge of them can be verified by exact observation.

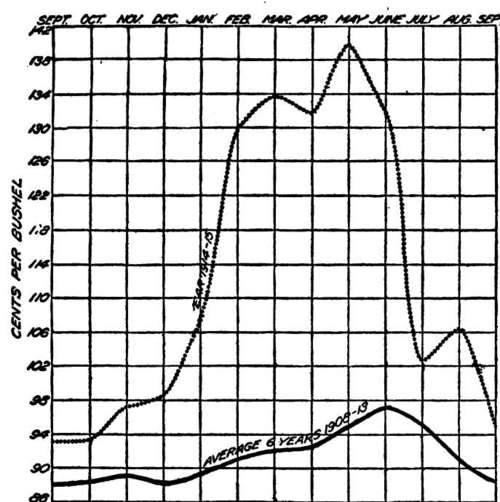

Possibly you have seen at some time or other, a chart indicating the trend of the stock or grain markets. A piece of paper is squared off in blocks, each row representing a cycle of time, usually a year, and across these blocks there will be a wavy line running either longitudinally or perpendicularly. This line is supposed to trace the trend of prices. Figure 4 shows a chart which might be used as a powerful argument for always buying May wheat in September. Such charts have many followers who foolishly believe they can replace judgment with a greater degree of accuracy. But they more frequently go wrong than right. They might be accurate guides were similar conditions always present; the charts would indicate a recurrence in a swing in prices upward or downward as the case might be, but this is not always the case, fate having a strange inconsistency in bringing forward unexpected events which wholly change the course of human expectations.

It does not follow that a system of charts or diagrams based upon business fundamentals and currently revised with intelligence and discrimination may not serve a useful purpose. In fact, economic science and statistical work of various kinds are gradually making possible the compilation of information possessing great value. No system of charting or of presenting such information can, however, entirely forecast the unexpected events.

Fig. 4. Chart Showing the Average Price of Wheat.

Continue to:

My Books