138. The Credit Department

Description

This section is from the book "Money And Banking", by John Thom Holdsworth. Also available from Amazon: Money And Banking.

138. The Credit Department

The credit department is one of the most recent, yet most important in the organization of the modern commercial bank. In the large city bank having a great variety of customers and activities, it is indispensable, and even in the small country bank, credit information regarding its customers, carefully collected and filed for ready reference, is highly desirable. Formerly the cashier was supposed to be sufficiently informed upon the business standing and credit of all the bank's customers, but to-day the larger banks find it necessary to have highly organized credit departments in charge of a specialist whose chief or sole duty is to accumulate and make easily accessible credit information regarding nil customers of the bank. Where loans are conservatively made on high-grade collateral security the question of credit is not so important, but in the case of the discount or purchase of commercial paper resting upon personal credit the financial responsibility and character of the borrower is a matter of first importance.

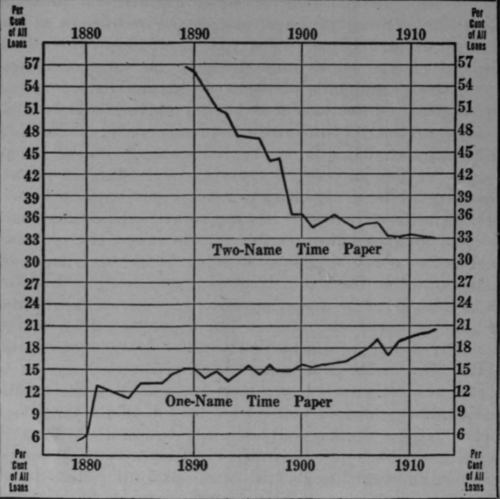

The Trend Toward Personal Credit

Chart Showing Relative Importance of One-name and Two-name Paper.

Courtesy of The Annalist

The credit man should keep complete records regarding mortgages, judgments, assignments, petitions in bankruptcy and like matters affecting the bank's customers. He should have available the financial history, the present standing, and the habits of life and character of every borrower. He should also keep posted on the general conditions of business. In aiding the lending authorities of the bank to determine whether credit shall be extended to a borrower and to what extent, the credit man should be able to present facts concerning the character of the business, its form of organization, its management and business methods, the extent of competition, the promptness with which bills are paid, the financial worth of the business, the extent of borrowing at other banks, business reputation among other people, etc.

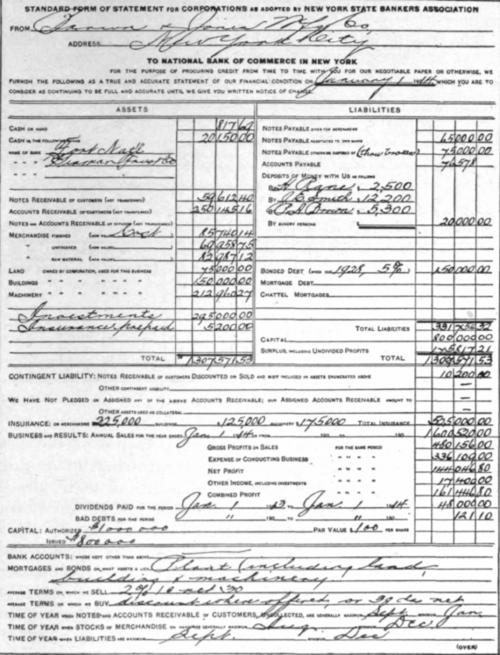

Borrower's Statement - Front.

The credit man obtains his information from various sources, the chief source being the statements of the customers themselves. The practice is growing of requiring borrowers to make a full statement of their affairs when they apply for a loan. Uniform blanks have been adopted by the bank associations of several states. Some banks require applicants to make oath to their statement. In some of the states laws have been passed making it a criminal offence to obtain loans on false or misleading statements. Sometimes the banks require the statement to be certified by a public accountant. Separate forms are used for individual borrowers, for firms, for corporations, and for banks. Shorter forms are sometimes used when minute details are not deemed necessary.

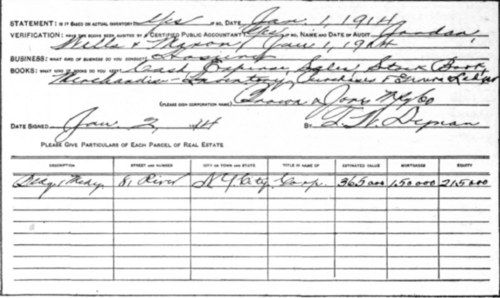

Borrower's Statement - Back.

These statements call for detailed information regarding the resources and liabilities of the applicant, including such typical assets as: cash, merchandise in both the raw and manufactured form, bills receivable, accounts receivable, plant, machinery, equipment, real estate, franchises, treasury stock, etc.; and such liability items as bills payable, accounts payable, stocks, bonds, mortgages, depreciation, net worth, net earnings. The ratio of quick assets to the two important liability items - bills payable and open accounts - affords a rough basis for determining the commercial standing of the borrower. One dollar of indebtedness to a dollar and a half of quick assets is usually regarded as a safe proportion.

Other sources of information are the mercantile or credit agencies, the most important of which in this country are Dun's and Bradstreet's. It is the business of these credit agencies to collect and summarize credit information regarding all kinds of business concerns all over the country. Though the banks do not depend very largely upon these agency reports, they are valuable in suggesting credit information that might otherwise be overlooked. Such reports should always be supplemented by personal investigation.

The signed statements, agency reports, letters, memoranda, and credit information of all kinds are tabulated, analyzed, and filed in the credit department in readily available form. New statements are required from time to time as borrowers apply for new loans or as paper is offered for discount. In the case of regular borrowers banks may require statements only at regular intervals, for example, once, twice, or four times a year. In this way the banks will have after a time a series of statements from borrowers showing the changes in their business.

In the bank having a well-organized credit department every application for a loan or offer of commercial paper is referred to the credit man. After investigation he prepares for the loaning officers a condensed statement showing the essential facts affecting the applicant's credit. Upon the basis of these facts mainly is determined the granting or refusing of credit accommodations by the bank.

Continue to:

My Books