Chapter 6. Rising Prices And The Standard

Description

This section is from the "Economics In Two Volumes: Volume II. Modern Economic Problems" book, by Frank A. Fetter. Also available from Amazon: Economic

Chapter 6. Rising Prices And The Standard

§ 1. Rising prices, 1896-1913. § 2. Rising prices in Europe, 1914-1920. § 3. Causes of European inflation. § 4. Gold stocks of belligerents. § 5. Redistribution of European gold stocks. § 6. The flood of gold to America, 1915-1917. § 7. The gold embargo in the United States. § 8. Gold depreciation and gold production. § 9. The high cost of living, 1919-1920. § 10. Various ideal standards suggested. §11. The tabular or multiple standard. § 12. Fluctuating standard and the interest rate.

§ 1. Rising prices, 1896-1913. The free-silver advocates got what they desired, a reversal of the movement of general prices, through an occurrence for which no political party could justly claim the credit. In 1883 the gold production of the world was less than $100,000,000. From that date, with the opening of new gold-yielding territory in South Africa and in the Klondike, the annual output of gold had been increasing rapidly and almost steadily. The methods of extracting gold theretofore had still been in large part of a primitive sort. But intricate machinery was taking the place of crude tools, chemical processes had been introduced (notably the cyanide process), and the principal product began to come from the regular and certain working of deep mines rather than from chance surface discoveries. In many parts of the world there were enormous deposits of low-grade ores, before useless, that could be worked economically by the new methods. It is noteworthy that the very year 1896, which marked the height of the political agitation to abandon the gold standard for silver, saw the gold production for the first time in all history surpass the $200,000,000 mark. The gold output had not only caught up with, but had begun to surpass, the normal monetary demands of the world, meaning by that phrase the amount of gold needed to maintain a stationary level of prices.

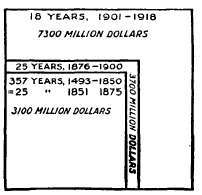

A study of Figure 1, chapter 6, will help to an appreciation of the enormous increase in the world's production of gold after 1850. The production of gold from the discovery of America to 1850 doubtless was much greater than it had ever been in any equal period. But this amount was duplicated in the next quarter of a century, again duplicated in the next twenty-five years, and more than doubled in the following eighteen years. The annual average output in the 357 years ending 1850 was $8,700,000, in the quarter century following 1850 was $124,000,000, from 1876 to 1900 was $140,000, 000, and from 1901-1918 was $405,000,000.

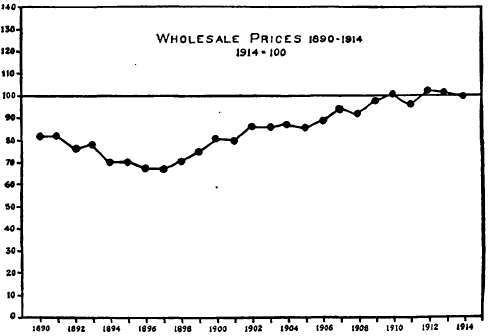

The whole character of the monetary problem was changed. A period of rising prices set in, as is shown graphically in Figure 2, chapter 6. By 1913 prices had risen just about 50 per cent above the low level of 1896. The rise was at the average rate of nearly 3 per cent each year. This caused a reversal of the former positions of advantage and disadvantage on the part of debtor and creditor respectively. The burden of the average debt began relatively to decrease. A wide field for enterprisers' profits was opened up by the rapid displacement of prevailing prices in all quarters of the industrial world. The price of manufacturers' products rose in advance of the rise of costs of many raw materials and especially of the labor costs of manufacture. The average enterpriser's gain was the average wage-worker's loss. Wages (and salaries), as nearly always in the case of a change of price levels, moved more slowly than did the prices era in price history, and is now usually taken as the base from which are measured in the various countries the remarkable series of price changes that followed. The year 1914 was one in which the political outlook was disquieting, and the European state banks and treasuries were quietly building up their gold reserves to meet possible emergencies, thus of most of the commodities that are bought with wages, thus causing great hardship to large classes living on comparatively slowly moving incomes.1 Extremes meet, and these classes include both those living on passive investments and those dependent on their daily labor for a livelihood.

Fig. 1. Gold Production by Periods

1 This happened to coincide with a relative increase of the prices of food-products and of other necessities of daily life at a greater rate than general prices. This aspect of the much-discussed rising cost of living must be carefully distinguished from that of the change of the general price level, and also from that of the relatively slower change of wages. See Vol. I, pp. 437, 445-446 on population and food supply.

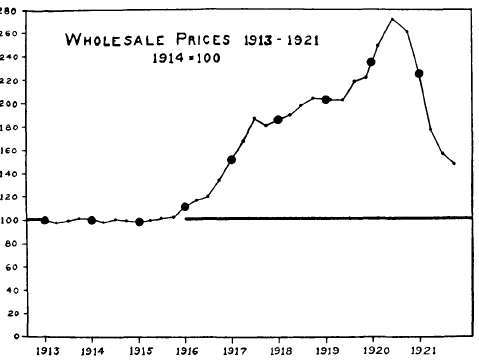

§ 2. Rising prices in Europe, 1914-1920. The year 1913, the last before the outbreak of the World War, marks a new contracting the circulation. The annual average index numbers in all the leading countries were nearly the same in 1914 as in 1913.

Fig. 2. Wholesale Prices in the U. S., 1890 -1914.

In the "warring countries, however, wholesale prices began at once in August to rise rapidly, attaining in the last quarter of 1914 the figure of 107 in France and 108 in Great Britain. "Retail price changes in every country lagged behind the wholesale, not infrequently being retarded a year or more. This rise of prices continued, with hardly an interruption, in all countries, reaching the maximum about the middle of 1920.

In the United States prices fell quickly to 98 in the last quarter of 1914, as gold was clamorously (and foolishly) demanded by European bankers, and a brief financial panic occurred. But the average of prices continued in the United States almost stationary until the last quarter of 1915 (that is, about one year after the war began in Europe), when they began to rise sharply, for reasons that will be indicated in the next section. The changes are shown graphically in Figures 3 and 4, Chapter 6.

Fig. 3. Wholesale Prices in the U. S., 1913-1921.

Continue to:

My Books