Crises And Industrial Depressions. Part 2

Description

This section is from the "Economics In Two Volumes: Volume II. Modern Economic Problems" book, by Frank A. Fetter. Also available from Amazon: Economic

Crises And Industrial Depressions. Part 2

§ 6. A business cycle. Let us now sketch in broad outline a business cycle bearing in mind that this series of changes does not repeat itself with unvarying regularity, but that it is fairly typical in the modern business world. The period leading up to a crisis is one of relative prosperity; then occurs a crisis in which prices fall, at first rapidly, and afterward for a while going slowly lower. When prices are at the lowest point many factories are closed and much labor is unemployed. Let us start at that point. Conditions are worse in some industries than in others. General economy and great caution prevail; few enterprises are undertaken. For those persons having available funds this is a good time to buy, and property begins to change hands. Then hoarded money begins to come out of its hiding-places. Money and credit flow in from other countries, particularly if business conditions are better abroad than here, for when prices are lower than they have been, relative to those of other countries, a country is a good place in which to buy. At the same time that the money in circulation thus increases, there is a general return of confidence that increases credit. Not only are there more dollars, but each does more work. Then old enterprises are resumed and new ones are undertaken. The purchase of materials in larger quantities causes a rapid rise in the prices of many raw materials and of all kinds of industrial equipment. The less efficient laborers and others that have been out of work begin to find employment, and then, more tardily, wages begin to rise. As a result, the costs of many products begin to rise rapidly. The only classes not sharing in this improvement are the receivers of fixed incomes. As prices rise, the purchasing power of their incomes correspondingly falls.

6 See ch. 6, § 9; ch. 9, § 13.

At length prices begin to go up less rapidly, and the question arises in many minds whether the movement can continue, and if not, when it will cease. Men wish to hold on for the last profits, and are willing to risk something to gain them. When prices rise not only as compared with former domestic prices, but as compared with current foreign prices, foreign imports are stimulated and exports fall. This calls for a new equilibrium of money, and requires at length large and continued exportation of specie. This checks prices, and, reducing the specie reserves of the banks, compels them to be more cautious. At the same time the increase of costs in many industries begins to reduce profits. The fall in the value of many stocks and securities held by the banks forces many brokers and speculators to convert their resources into ready money. This is the moment of danger; weak enterprises find their foundations crumbling, and there are many failures.7 The falling prices, the shattered credit, and the financial losses force many factories to close, and many workmen are thrown out of employment. This period of beginning collapse is the crisis. It is followed by another period of low prices and of small output, and therefore of profits small or negative in many industries. Business must again enter upon a period of retrenchment, for it has completed another cycle.

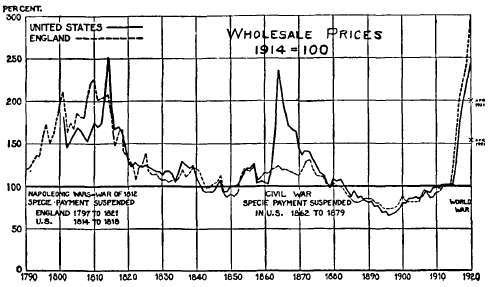

Fig. 1, Chapter 10 shows the great similarity in the changes of general prices in England and in the United States from 1790-1920, both in respect to the larger movements and levels, and to the minor fluctuations. It shows also that this relationship has become much closer since 1870. See also Figure 1, Chapter 5.

§ 7. General features of a crisis. Although irregular in time of occurrence and unlike in their immediate occasions, financial crises show certain general features. They are a part of the larger movement here outlined as the business cycle. Some have thought this cycle to be normally a period of ten years, divided into one year of crisis, three years of depression, three years of recovery, and three years of unusual prosperity. This succession of events occurs pretty regularly, though not in the regular intervals of time. Crises are more severe in countries with more extensive use of money and credit, but still more severe where the credit system is more loosely administered and less efficiently coordinated. As a rule they have been harder in the United States and England than in Germany, harder in Germany than in France, harder in western Europe than in eastern Europe, harder in Christendom than in heathendom. They are less severe in rural districts, where prosperity depends more on crop conditions and business has in it less of financial speculation. Their effects are least felt in the staple industries, for when hard times come people economize on the less essential things. The glove factory, the silk factory, the golf-club factory are more likely to close than is the flour-mill. In a crisis wages and salaries are less quickly affected than are profits, but wageworkers suffer in the loss of employment. Those money-lenders who have eliminated chance as far as possible and have taken a low rate of interest lose little; the risk-takers who draw their incomes from dividends on stock or from bonds of a less staple kind often lose much. § 8. The use of credit. The general use of credit is, as we have observed, an essential condition to the occurrence of a financial crisis, so that, indeed, a crisis might be called a disease of the credit system. The use of credit greatly enhances the rhythm of price. If the value of a thing that is fully paid for falls, the owner alone loses; but if the value of a thing only partly paid for falls so much that the owner is forced to default in his payment, the loss may be transmitted along the line of credit to every one in a long series of transactions. A credit system, highly developed, is a house of cards at a time of financial stress. Demand liabilities are at such a time the greatest danger, so that the banks, ordinarily the pillars of financial strength, become at such a time the points of greatest weakness in the financial structure. If many of the customers were not restrained by their sense of personal obligation to the banks, by the strong pressure that the banks can bring to bear upon them, or by the force of public opinion among business men, from withdrawing the balances to their credit in a time of crisis, all commercial banks would become insolvent at once in a crisis by the very nature of their business; for all their ordinary deposits are nominally payable on demand.

7 See diagram of business failures, 1890-1914, in Vol. I, p. 364.

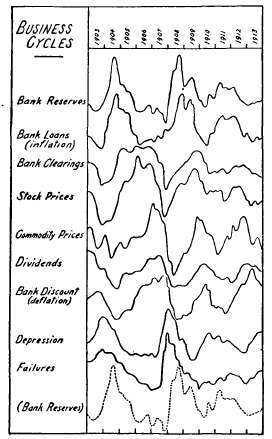

Fig. 2, Chapter 10, on Business Cycles, shows the rhythmic movement that occurs in various business and financial conditions. Taking the curve of commodity prices aa the central fact, it is seen that its peak has been preceded in time successively by peaks of bank reserves, loans, and clearings, and by stock prices (which always speculatively anticipate higher dividends) and is soon followed by declining dividends, by the peak of discount rates, and by failures; then bank reserves gradually being built up, the cycle is repeated. This diagram, hitherto unpublished, was prepared by Professor G. R. Davies, University of North Dakota, to whose courtesy we are indebted for permission to use it here. The data are plotted so as to show the variations above and below the averages, eliminating the absolute growth due to increasing population, business, etc.

Continue to:

My Books