Studio Bookkeeping. Part 2

Description

This section is from the book "Complete Self-Instructing Library Of Practical Photography", by J. B. Schriever. Also available from Amazon: Complete Self-Instructing Library Of Practical Photography.

Studio Bookkeeping. Part 2

716. Recording The Sitting

Recording The Sitting. The order for the sitting may be recorded before the customer is photographed, but usually it is better to make the sitting first and then register him afterwards. There is an advantage in registering the customer after the sitting is made, in that after the pains taken in making the sitting the customer feels pleased

Illustration No. 92 Receipt Book.

See Paragraph Ha 717 and it is much easier to obtain a deposit, as the negatives are already taken and there is no chance to refuse even if he or she were so inclined. Therefore, we would recommend the registering of the customer after the sitting is made.

717. Receipt Book

Receipt Book. A receipt should always be given when payment is made. A very good form is shown in Illustration No. 92. A convenient size receipt blank would be one about 5 1/2 x 3 1/4. These receipts, of course, should be printed and it is an excellent plan to have them bound in pads with a blank sheet of light yellow paper between each receipt. A sheet of carbon transfer paper should be placed between the receipt and the blank yellow sheet of paper. In this way a perfect duplicate of the receipt will be made on the blank sheet, and when the original receipt is torn off and given to the customer you will have a record of it in your stub book.

718. As will be seen a little later, this duplicate receipt in your book will be of vital importance for this particular system, as it gives you the record without its being necessary to copy it a second time; therefore this form requires but one transcript in addition to the original record in registering. The customer is instructed to present the receipt when calling for proofs (unless they are mailed out), and also when calling for the photographs, for this will avoid delays and misunderstandings. The receipt contains a complete record, the name of the customer, the date they sat, the number of their order, the number of pictures originally ordered, the style, total price and the amount paid. This is all the entry that is made at this time until the proofs are returned and the final order given.

719. When the proofs are returned a record should be made in the studio register of the date, and also the date when pictures are promised. It is customary to promise delivery of pictures in two weeks. The total length of time, however, is not at all arbitrary and may be determined by the photographer. Under no circumstances, however, promise pictures before you know conscientiously that you will be able to deliver them. When you make a promise keep it. If there is any change in the amount of the order the item may be inserted directly above the one already placed in the register. For instance, referring to Illustration No. 91, Miss Mary Miller, under order No. 35541, desires to have a dozen pictures, but wants them finished from three negatives. A charge of 50 cts. is made for each additional negative, therefore, the amount of $1.00 should be inserted directly above the $4.00. The total amount of her order is, therefore, $5.00. As she has made a $2.00 deposit, the balance due is $3.00, which amount is to be paid on delivery of the pictures.

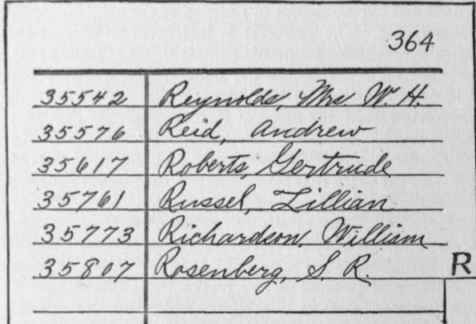

720. When the pictures are delivered, the balance to be paid on the order, which will be the difference between the total amount of the order and the amount originally paid, should be inserted above the amount paid. For example, Order No. 35542 of Mrs. W. H. Reynolds, for $80.00. She paid a deposit of $2.00 and when she received her pictures she paid the balance, $18.00, and this amount was placed above the $2.00. This balanced Mrs. Reynolds'

Illustration No. 03 Index Book - Alphabetically Arranged.

See Paragraph No. 721 account and she was given a receipt for the amount, a carbon copy of which remained in the receipt book. By checking up your carbon receipts with the register, you at once see that the pictures were delivered and the full amount of the account was paid, and by checking your carbon receipts with your cash they must balance, thus giving you a record of all your business. By handling the studio business in this way there is little bookkeeping and practically but one record to be made, the record being complete in every respect.

Continue to:

My Books