International Trade. Part 4

Description

This section is from the "Economics In Two Volumes: Volume II. Modern Economic Problems" book, by Frank A. Fetter. Also available from Amazon: Economic

International Trade. Part 4

§ 9. Cancelation of foreign indebtedness. In the inter national business of any two important countries to-day, such as England and America, the number of credit and debit transactions is enormous. If each trader had to attend to the forwarding of the means of payment for his purchases, he would, of course, deduct from the amount of his indebtedness the amount due him from his foreign correspondent, and might from time to time "remit" the balance in the form of a shipment of gold. This simple offsetting and cancelation of debits and credits would greatly limit the amount of gold that would have to be shipped. But still, under such conditions, there must be a very large number of shipments of gold by different individuals, and a large proportion of these shipments would be going in opposite directions at the same time. Now, a merchant in New York called M may have a balance to pay in London to X, and at the same time a merchant in London called Y have a balance to pay in New York to a man called N. If M can buy from N his claim in the form of an order, draft, or bill of exchange, and send it to X, the latter may through his bank collect the sum from Y. In this way a further cancelation r,f indebtedness would occur.

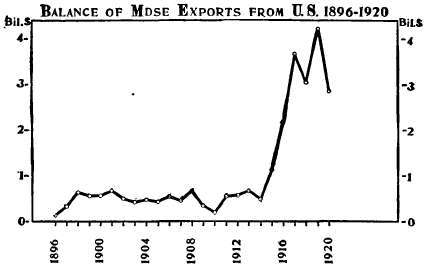

Fig. 2, Chapter 15, shows in more detail, by years for 1896 to 1914, on a different scale, the facts for which Figure 1 shows only the averages.

When all persons having either debits or credits to be paid in New York and in London, respectively, are dealing with the banks in these cities, and the banks and special exchange brokers are constantly buying and selling these bills, a market is created for London exchange in New York (and conversely in London), and a much easier and more nearly complete cancelation of indebtedness results. In effect, all the debits and credits between the two countries are merged into one big ledger balance, and the international shipment of gold bullion finally made is just the amount needed to balance the accounts payable at the time. Industrial indebtedness is represented in various forms: bills of lading for goods shipped, drafts made by the creditor on his debtor for goods shipped or property sold, checks or letters of credit for travelers, bonds and notes public and private. These are the objects dealt in by the bankers who are the agents to carry on the work of exchange.

The balance of foreign exchanges is of essentially the same nature as the domestic cancelation of indebtedness. It is going on constantly between the two merchants in the same town, between two banks in the same town who represent groups of merchants, between men in neighboring towns, and between distant states like New York and California.6 The price of exchange to the individual is reduced by the specializing of the business in the hands of a few dealers, permitting the cancelation of indebtedness or offsetting of exchange, and greatly reducing the amount of bullion to be transported in making the payments. The cost to the bank of providing this exchange for its customers varies as conditions change, but in any case is not great, so that in domestic business when any charge is made it is usually at a fixed rate, and is mainly for the service.

6 See ch. 7, sec. 8.

§ 10. Par of exchange. Foreign exchange from America to Europe is, however, in two features different from domestic exchange: (a) the cost of shipment of gold is greater; (b) the monetary units of the two countries usually differ in name, weight, and fineness, and sometimes in materials. "We may define foreign exchange as the purchase and sale of the right to receive a given kind and weight of metal or its monetary equivalent in current funds at a specified time and place, or as the funds so purchased. Par of exchange between two countries using the same metal as a standard is the number of units of the standard coin of the one country that contains the same amount of fine metal as the standard coin of the other country. There is no fixed par of exchange between gold-using and silver-using countries; par of exchange between them fluctuates with changes in the comparative values of the two metals. The gold-shipping points for importing or exporting gold are respectively par of exchange plus or minus the cost of moving the actual metal. These points vary with means of transportation and communication. The par of exchange between New York and London being nearly $4,866 and the cost of expressing and insuring a gold pound between New York and London being approximately $.02,7 the shipping point for the export of gold from New York is $4,886 and for the import of gold to New York is $4,846. At these upper and lower limits, there is a motive for shipping gold as a commodity.

"When large sales have been made to Europe and credits are accumulating in New York and the importation of gold is imminent or already begun, the claims are bought by bankers in New York at less than par. At such a time one needing to remit a sum to London can buy exchange for less than par, for every such draft remitted reduces London's indebtedness and, by so much, the need of shipping gold to this country. As a rule, then, accumulating credits here mean a low rate of exchange, accumulating debits a high rate of exchange from this to the foreign country.

7 This varies also with conditions; after the outbreak of the war in 1914 it was for a time as high as $.05 because of high war rates of insurance.

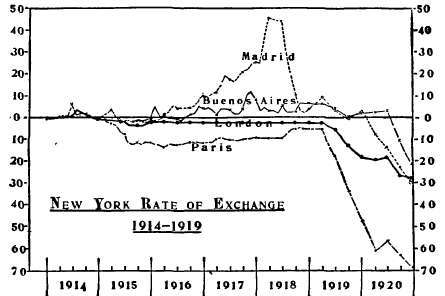

Fig. 3, Chapter 15, shows the variation of New York rates of foreign exchange with four financial centers in the very abnormal period from 1914-1020. Exchange below par (0) indicates large purchases from the United States, (the case of English and French exchange from the end of 1914). Exchange above par (Spain and Argentine, 1917-1919) indicates large purchases by the United States while the embargo policy was in effect (see Chapter 6).

These are the merest rudiments of the subject. The many problems arising, such as the adjustment of foreign credits to changing needs, and such as arbitrage (the readjustment of the rates of exchange prevailing among different financial centers), make foreign exchange both a complex science and a difficult art.

§ 11. International monetary balance and price levels. The balance of all accounts for or against a country (including new loans, current interest, and repayments) must thus eventually be settled in money. This cannot fail to effect the general level of prices in both countries, though this is brought about often only in indirect and gradual ways. The flow of money out of a country causes the loan market of a country to tighten (interest and discount rates to rise) in proportion as the reserves of the banks are reduced. Then "general prices" begin to fall.8 When prices fall, imports decline, as the country is not so good a place in which to sell: when prices rise, imports increase, as it is a better place in which to sell. The opposite effect is produced on exports, and thus in a short time the national credits and debits are again brought into equilibrium. A slight movement of money in either direction is enough to influence prices and set in motion forces to counteract a further flow of money. Decade after decade the circulating medium of loading countries changes very slightly in amount, and the fluctuations in its amounts during periods of so-called "favorable balance of trade" and of "unfavorable balance of trade" are only the smallest fraction of the value of goods passing through the ports of the country.

It is therefore absurd to imagine, as is sometimes done, that a country could continually import goods until it was drained of all its money, or that by any possible set of devices it could forever have an excess of exports to be paid for by a continual inflow of gold. Long before either of such movements could go far, the automatic readjustment of international prices would inevitably check it, and secure and retain for each country its due portion of the money.

8 The connection between a high rate of interest and falling prices is a dynamic phenomenon of a very temporary nature. In long-time static conditions the general level of prices and the prevailing rate of interest are dependent on entirely different sets of forces. See on the theory of interest, Vol. I, p. 308. In long-time movements of prices, in contrast with brief changes due to foreign trade such as are referred to above, high rates of interest are connected with rising prices, and vice versa. See above, ch. 6, § 12, on fluctuating price levels and the interest rate.

References

Bastable, C. E., The theory of international trade. N. Y. Mac millan. 1903. Brown, E. G., International trade and exchange. N. Y. Macmillan.

1914. Clare, G., The A B C of the foreign exchanges. N. Y. Macmillan.

1895. Escher, Franklin, Foreign exchange explained. N. Y. Macmillan.

1917. Goschen, Viscount, The theory of the foreign exchanges. N. Y.

Scribner. 1898.

Continue to:

My Books