Section 27. Property Ledger, City Properties

Description

This section is from the book "Real Estate Accounts", by Walter Mucklow. Also available from Amazon: Real Estate Accounts.

Section 27. Property Ledger, City Properties

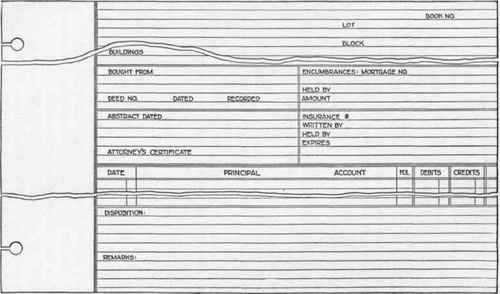

It is beyond question that the most convenient form for the record of city properties is a loose-leaf book. As already stated, the property ledger shown in Form 21 is suitable for this purpose, as is also the city property ledger shown in Form 25. The latter form provides for the entry of all essential information and is almost self-explanatory.

Particulars as to appraisals and selling price may be entered in the "Remarks" division, while expense and receipts maybe put on the back as memoranda.

The most convenient method of arranging this ledger is to keep together all sheets relating to the same subdivision, arranging them in alphabetical or geographical order as may be desired, and separating them by blank sheets of heavy paper, to each of which is attached a movable index tag giving the name of the plat referred to on the sheets following. This method gives immediate access to the records of any piece of property of which the description is known. If the name of the vendor is known, reference to the property index (Form 19) will give the subdivision; while, if only the street address is known, the property can be located by means of the rent record given in Form 32 (Section37).

Such an arrangement assists an auditor materially, as it insures against the duplicate entry of any piece of property and provides for the entry of all mortgages on any property in one place - matters which could not be determined under any other arrangement without much search.

To illustrate, let us suppose that a piece of property is described in several ways, such as "part of lot," or "north ½ of lot," or by metes and bounds. Quitclaim deeds to the property may be obtained, in each of which a different form of description is used. If the property ledger is arranged in the order of the dates of deeds, or in alphabetical order by the names of grantees, separate mortgages might be entered under the several descriptions, and one or more might escape even a careful checking.

When writing up the property ledger sheet for any improved property, care should be taken to enter separately the value of the land and the value of the improvements, even if this division of the cost must be approximated. This information is necessary for insurance purposes, and also in connection with tax matters, and to determine whether or not depreciation should be charged - .something" considered more fully under "Depreciation" (Chapter XXXII (Depreciation. Section 315. Depreciation Of Realty)).

Form 25. (a) City Property Ledger (face).

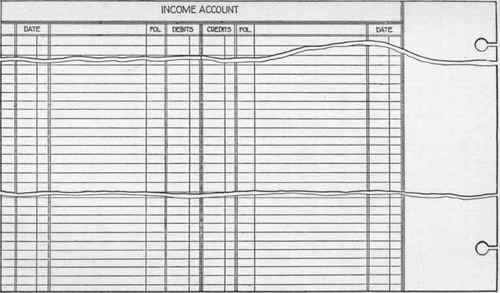

Form 25. (b) City Property Ledger (back).

Form 26. Property Ledger - English Form.

It not infrequently occurs that land bought and entered as wild land, or as a city block, is subsequently subdivided and replatted into small parcels. If the subdivision contains a large number of lots, it is not necessary to enter each separately on the property ledger, as they can better be recorded on the plat books and ticklers discussed in SectionSection 29, 30.

If comparatively few lots result from such subdivision or replatting, it may be advisable to carry each lot in the property ledger on its own account. In such case, the original account in the property ledger is closed by a journal entry and new accounts are opened, one for each lot of the subdivision, care being taken to divide properly the cost among the new subdivided lots.

The property ledger shown in Form 26, given as an alternative method of recording property, is entirely different from the property ledgers already shown. It was designed for English practice - a fact which accounts for the small space reserved for rents, which in that country are generally paid quarterly.

Continue to:

My Books