Insurance

Description

This section is from "The Domestic Encyclopaedia Vol3", by A. F. M. Willich. Amazon: The Domestic Encyclopaedia.

Insurance

Insurance, in law and commerce, denotes a contract by which one party engages to pay the other, for a certain premium or consideration, such losses as he may accidentally sustain. The common kinds of insurance are :

I. Against loss at sea ; a most beneficial institution, eminently calculated for promoting the security of trade. It is at present conduct-ed by a regular system of rules, under the immediate sanction of the law, the decisions of courts of justice, and the usage of merchants. There are several societies for this kind of insurance in London ; but, as it would be incompatible with cur limits to enter into any details, we shall point out Mr. PaRK's masterly System of the Law of Insurances (8vo. Butterworth, 12s. 18Ol) in which the subject is fully considered. A smaller work of reference, designed for the use of merchants, and relating to Insurance against Losses at Sea, has lately been published by Mr, Burn.

II. Against fire; for which purposes various offices are established in Britain : the principal or them is, probably, the Sun Fire-office. This class is divided into three species, namely:

1. Common insurances: buildings, the whole external walls of which are of brick or stone, with coverings of slate, tiles, or metals, and in which no hazardous trades are carried on, or hazardous goods are deposited. In this division are also comprised goods which are not hazardous, and which may be kept in such buildings.

2. Hazardous insurances, which include buildings covered with slate, tile, or metal, whether built of timber, plaister, timber and plaister, brick and timber; and also buildings, the external walls of which are not wholly of brick or stone, and in which no hazardous trades are carried on, or hazardous goods are deposited : and brick or stone buildings with the coverings above-mentioned, containing hazardous trades or wares.- Also goods, deposited in all timber, plaister, timber and plaister ; and brick and timber buildings; hemp, flax, pitch, tar, cotton, turpentine, resin, oil, spirits, and the like, are classed among hazardous insurances, as likewise are the trades or manufactories using the last-mentioned articles.

3. Doutly hazardous insurances: namely, all the buildings mentioned in the preceding section, however covered, if they be occupied by hazardous trades or goods ; and all thatched buildings.

Ships, vessels, barges, and other craft, together with their cargoes j glass, china, earthen-ware, pottery, bottles, bottled liquors in trade, ornaments, shells, fossils, ores, medals, curiosities, oil of vitriol, cork, statuary, and figures in wax, plaister, and marble; are all included in this subdivision, to which may be added the. trades of boat-builders, cart-grease-makers, cork-cutters, varnish, flambeau, and lamp-black-makers, hartshorn and vitriol works, oil, silk, and linen manufacturers, and japanners.

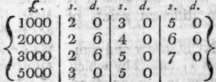

Such are the species into which insurances against tire are divided: and that our readers may form some estimate of the expence of insuring goods, etc against loss or damage by fire, we have subjoined the fo lowing brief table, in which the different annual rates, payable at the British Fire-office in the Strad, may be seen at one view.- Beside these rates, however, there is a duty of three shillings to be paid to government, for every policy of insurance where the sum insured does not amount to 1OOOl.; and of six shillings, if it amount to 10001. or upwards.

Any sum not exceeding Common Hazardous. Doub Hazard per Cent

When the sum insured is large, a higher premium per cent, is demanded ; and money, papers, pictures, gunpowder, and jewels, are excluded.-r-If an article be falsely described, in order that it may be insured at a lower premium, the policy is justly void. An insurance made on the same subject at different offices, must be specified by indorsement on the policy; and, in case of loss, the offices pay a sum in proportion; as well as all the expences incurred in attempting to extinguish fire, or to saye goods, even though the endeavours should not be attended with success. And if the value of an article be partially insured, and receive damage by fire, the society is bound to make restitution only to the extent of the sum for which the premium is paid.

III. For lives by virtue of which, on the demise of the party insured.

a sum of money becomes due to the person for whose benefit the insurance was made. In this respect also, several societies grant policies of insurance for certain premiums : and, though our limits do not allow us minutely to specify the rules and rates of computation which different associations have adopted, yet we think it will be useful to exhibit a few particulars relative to the premiums paid by persons, who insure either their own lives, or those of others in which they have a certain interest. In the following table we have stated the rates of insurance on lives, fixed by the Westminster Society (No. 429, Strand), which was established in 1792 : it is calculated to shew the premiums for insuring one hundred pounds, upon the life of a healthy person, from the age of eight to sixty-seven years, within the limits of Europe, but not upon the seas, viz.

Age.

Premium | per | Premium per | Premium per | ||

cent, for one | cent, per an- | cent, per an- | |||

Age. | year. | num, for an insurance for seven years. | num, for the whole continuance of life. | ||

£. s. | d. | £'. s. d. | £. s. d. | ||

8 to 14 | 0 \7 | 9 | 1 1 5 | l 17 7 | |

20 | 1 7 | 3 | 1 9 5 | 2 3 7 | |

25 | 1 10 | 7 | 1 12 1 | 2 8 1 | |

30 | 1 13 | 3 | 1 14 11 | 2 13 4 | |

35 | 1 16 | 4 | 1 18 10 | 2 19 10 | |

40 | 2 0 | 8 | 2 4 1 | 3 7 11 | |

45 | 2 6 | 8 | 2 10 10 | 3 17 11 | |

50 | 2 15 | 1 | 3 0 8 | 4 10 10 | |

55 | 3 5 | 0 | 3 12 0 | 5 6 4 | |

60 | 3 18 | 1 | 4 7 1 | 6 7 4 | |

65 | 4 15 | 2 | 5 10 10 | 7 16 9 | |

66 | 5 0 | 1 | 5 17 7 | 8 4 1 | |

67 | 5 5 | 6 | 6 5 2 | 8 12 1 | |

Thus, a life not exceeding the age of 30 years, may be insured for 1001. to be paid in case of death within one year, for -------Within seven years, by paying annually till the insured shall die, or the seven years be elapsed,

Whenever the death shall happen, by paying annually till that event ------

£ | s. | d. |

13 | 3 | |

1 | 14 | 11 |

2 | 13 | 4 |

Another method of insuring for the benefit of survivors, consists in paying an annual premium for a certain sum recoverable on the death of one person named out of two; but, as this mode of securing a competency is doubtless more objectionable to the party that is obliged to pay the annual premium, than either the preceding simple, or subsequent double chance of obtaining an equitable reimbursement, we have been induced to subjoin the following table, which exhibits the premium of insurance of one hundred pounds, payable when either of (wo persons shall die within the limits of Europe, but not upon the seas.

10 | 2 | 17 | 1 | 40 | 5 | 11 | 9 | |

15 | 3 | 5 | 0 | 45 | 6 | 7 | 4 | |

20 | 3 | 13 | 11 | 50 | 7 | 7 | 8 | |

25 | 4 | 0 | 10 | 55 | 8 | 12 | 2 | |

30 | 4 | 8 | 11 | 60 | 10 | 4 | 9 | |

35 | 4 | 19 | 0 | 67 | 13 | 15 | 8 |

We have purposely omitted, in this table, the intermediate as well as the unequal ages of the parties whose lives are jointly insured; because the reader will be enabled to form a sufficient idea of the different rates, by comparing the present abstract with that of the preceding calculation.- Lastly, the same duties are imposed by government for insurance on lives, as those we have mentioned against losses by fire,

Continue to:

My Books